Just2Trade is here again and is ready to provide you with some useful information about cash flow, its types, tips on how to calculate cash flow and how to improve it, why it's actually important, and much more. Let's take a closer look at all the key details together!

Cash flow is the amount of money coming into and going out of your organization during a given period.

Cash flowing into the firm is the amount of money generated by sales, returns on investments, loans, etc.

Businesses also spend money on goods and services, utilities, taxes, loan payments, and other expenses; this is known as cash outflow.

Cash flow is calculated by comparing the amount of money that enters a firm over a certain time period to the amount that leaves that business over the same time period. Typically, a month or a quarter is used to measure cash flow.

A company's cash flow is the total sum of money coming into and going out of the company. Businesses that incur costs also receive income from sales. Investments, royalties, licensing agreements, and interest are other sources of income for them. In addition, they may offer items with the understanding that payment will come later.

Evaluating the quantity, timeliness, unpredictable nature, and sources and destinations of cash flows is one of the most important objectives of financial reporting. It's essential for figuring out how liquid, adaptable, and financially successful a firm is overall.

Positive cash flow indicates that a company's liquid assets are expanding, enabling it to fulfill obligations, reinvest in its business, distribute earnings to shareholders, pay costs, and serve as a safety net in case of impending financial troubles. Businesses can profit from beneficial investments when their financial flexibility is strong. As a result of not experiencing financial difficulty, they also perform better during recessions.

Analyzing cash flows can be done using a cash flow statement, a common financial statement that shows the sources and uses of cash for a business over a certain time period. It can be used by investors, analysts, and corporate management to evaluate how well a company can produce cash to pay off debts and manage operating costs. A cash flow statement is one of the most important financial statements a company issues, along with the balance sheet and income statement.

Now, let's have a look at the types of cash flow – below, you'll find all the key details about each one.

The term "cash flow from operations" (CFO), sometimes known as "operating cash flow," refers to financial transactions that are directly related to the manufacture and sale of goods. A company's CFO can tell whether or not it has enough money flowing in to cover its bills and operational costs. In other words, for a business to be financially viable over the long run, there must be more operating cash inflows than operating cash outflows.

To calculate operating cash flow, cash from sales is subtracted from cash spent for operational costs over the period. Operating cash flow is mentioned on a company's cash flow statement, which is displayed both quarterly and annually. Operating cash flow indicates if a company can generate enough cash flow to sustain and expand operations. It can also indicate when a company could require outside financing for capital growth.

Remember that the CFO can assist you in distinguishing between sales and cash received. For instance, revenue and profitability would rise if a company completed a big transaction with a customer. However, the additional revenue might not truly improve cash flow if there are issues getting the customer to pay.

The term "cash flow from investing" (CFI) or "investing cash flow" refers to a report that shows how much money was made or spent within a given time on various investment-related activities. Buying speculative assets, investing in securities, or selling securities or assets are all examples of investing activity.

If you experience negative cash flow from investment operations, it isn’t always a warning indicator and could be the result of considerable sums of money being spent on the long-term success of the business, such as research and development (R&D).

The term "financing cash flow," also known as "cash flows from financing," refers to the net cash flows utilized to finance a company's capital. Transactions, including the issuance of debt, equity, and dividend payments, are considered financing operations. Investors can learn about the financial health and cash flow management of a company's capital structure from financing activities.

Contrary to popular belief, profit is not the same as cash flow. These two concepts are frequently misunderstood because of how similar they appear to be. Keep in mind that a business's cash flow refers to the money coming in and going out.

On the other hand, profit is a specific metric used to assess a business's financial performance or total revenue. This sum of money is what's left over after a business settles all of its debts. Profit is what's left over after expenses are deducted from revenues in a business.

The simplest method for calculating cash flow is to use the following equation:

NET CASH FLOW = CASH RECEIVED - CASH SPENT

Your company sees positive cash flows and builds up cash in the bank if your net cash flow number is positive.

If your net cash flow statistic is negative, your company is experiencing negative cash flows and you are ending the month with less money than when you began.

A cash flow statement can be used in conjunction with other financial statements to calculate several metrics and ratios that analysts and investors can use to come to conclusions and make suggestions.

If their operating activities don't generate enough cash to maintain liquidity, even prosperous businesses may fail. This may occur if a company's profits are constrained by unpaid accounts receivable (AR), excessive inventory, or excessive capital expenditures (CapEx).

Because of this, creditors and investors want to know if the company has enough CCE to pay short-term obligations. Analysts look at the debt service coverage ratio to see whether a company can pay its current creditors with the cash it generates from operations (DSCR).

DEBT SERVICE COVERAGE RATIO = NET OPERATING INCOME / SHORT-TERM DEBT OBLIGATIONS (OR DEBT SERVICE)

But liquidity only provides limited information. A business may have a lot of cash because it is mortgaging its potential for future growth by liquidating its long-term assets or taking on unmanageable amounts of debt.

Free cash flow (FCF) is one of the metrics analysts use to gauge a company's underlying profitability. FCF is a very helpful indicator of financial performance and provides a richer narrative than net income since it reveals how much cash remains after dividends, stock buybacks, and debt repayment for business expansion and shareholder returns.

FREE CASH FLOW = OPERATING CASH FLOW - CAPITAL EXPENDITURES

Use unlevered free cash flow (UFCF) as a metric to assess a company's total FCF production. This measure of a company's cash flow, which excludes interest payments, reveals how much cash is available to the business before considering its debt. If there is a discrepancy between the levered and unlevered FCF, it can be determined whether the company is overextended or has a manageable level of debt.

The main goal of a cash flow projection is to foresee your future financial requirements.

Regrettably, anticipating your cash flow is a little trickier than forecasting your sales and expenses or other figures. If your company retains inventory on hand, your inventory purchase plans will also be used as inputs in your operating cash flow statement along with your revenue and expense estimates.

Additionally, you must project when your clients will pay you. Will they all do it on time? Or will some people take more time to pay?

Cash flow forecasting can be considerably facilitated by technology like LivePlan, but if you choose, you can also perform it manually using spreadsheets.

The direct method and the indirect method are the two approaches you can take when creating a cash flow statement. While they both forecast how much money you will have in the bank in the future and reach the same endpoint, they go about achieving that in different ways.

The direct method offers a very clear picture of how money enters and leaves a company. Basically, you total up all the funds that your company has received from different sources, then deduct all the funds that are distributed to suppliers, vendors, employees, etc. This figure represents the amount of money you added to or took out of your bank account during the month.

Starting with your net income from your profit and loss statement, the indirect method adjusts that figure to take into account non-cash expenses like depreciation. As a result, modifications are made to reflect inventory changes, accounts receivable, and accounts payable.

The indirect method is frequently used to construct historical cash flow statements, since your accounting system makes it simple to obtain all of the necessary statistics. This makes it a reasonably common way to predict cash flow, even if those who are less familiar with the complexities of accounting tend to find the direct method to be simpler.

Have there ever been instances where you attempted to pay for a company expense but lacked the necessary funds?

That actually indicates bad cash flow. It is also known as a lack of liquidity. Fortunately, there are actions you may take to improve liquidity and deal with any financial shortages.

It almost seems too obvious, but the more money your company receives, the more cash you have on hand to pay for bills.

Books, magazine articles, blogs, and your neighbor down the street all have advice on how to increase your income. However, when it comes down to it, there are only four strategies to boost revenue:

Boost the number of customers you have.

Increase the average sale amount.

Increase the frequency of purchases.,

Optimize costs.

So, for example, consider asking yourself, "How can I gain more customers?" instead of "How can I raise revenue?" The large issue of growing revenue is divided into manageable chunks when you use these four areas as a starting point, and you can then begin developing effective plans.

Similarly, cutting back on running expenses seems almost too obvious to mention. The bottom line will increase if you lower your cost of goods sold (COGS) and/or cost of services (COS). That might provide you with more money each month to work with.

Finding less expensive vendors, economizing, buying in bulk, or joining a buying cooperative are all positive steps toward reducing overhead. How you accomplish it will depend on your business.

The less cash you have on hand to spend, the more money is locked up in inventory; but, you must keep adequate inventory on hand to avoid running out and being unable to make sales.

Consider holding a sale if you're having a short-term cash flow issue. Sales are a great way to boost your company's cash flow right away and get rid of excess inventory, which addresses two issues at once.

Inventory management is an art, and can be impacted by things like company expansion, your marketing strategy, seasonality, and vendor prices.

Try to align your Accounts Receivable (receivable payments) with your Accounts Payable (outgoing payments). Let’s take the example of Tex, the owner of a restaurant for tourists. He could have purchased those funny souvenir hats if his customers had paid him promptly.

Say your loan installments are due on the fifteenth of each month. Your clients have 30 days to make payment after you invoice them. And on the first of each month, you send monthly invoices to the majority of your clients.

Because most clients wait to pay until the end of the month, by the time you have to make a loan payment, you still don't have your monthly income on hand. As a result, money is limited for the second part of the month.

This can be fixed. Altering the invoices' due dates or starting to send them out 30 days before each loan payment is due are two options. It’s usually easier, however, to call the bank and ask them to reschedule the date your loan payment is due.

The more liquid your assets are, the nearer they are to being cash.

Take Tex, for instance. You can't really exchange a mechanical bull for anything. Most definitely not for rent or to pay off debts. Cash, on the other hand, is useful in almost all circumstances.

You may have to sell your assets if you have a severe cash flow crisis and can't pay your bills on time or pay your employees, your mortgage, or your debts. It's a good idea to keep track of the assets you can sell at any given time. For instance, Tex is aware that he can sell one of his old mechanical bulls to a customer on eBay and make his necessary payments if things ever become very bad.

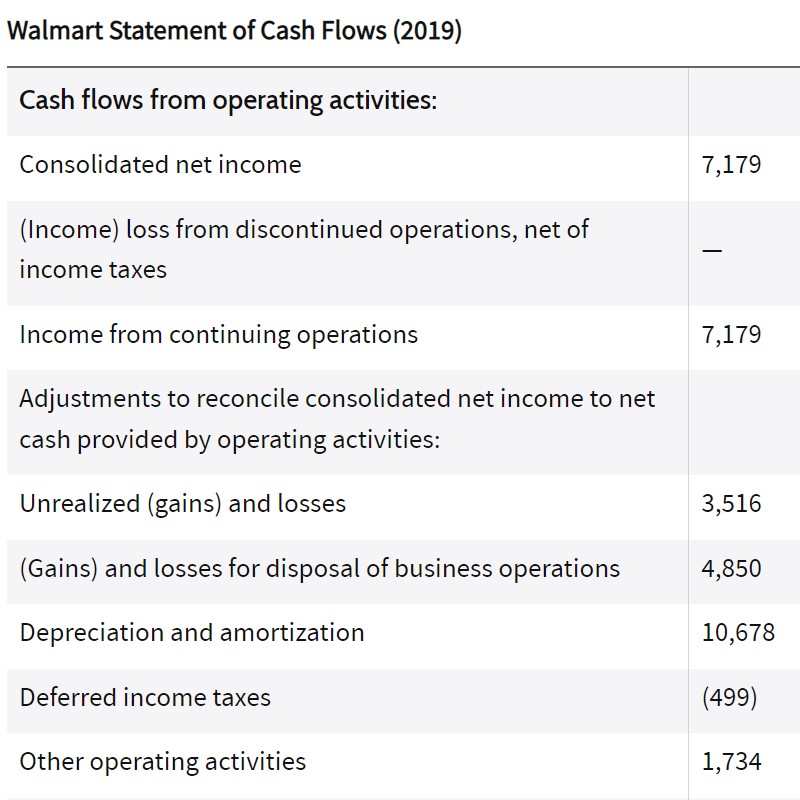

The cash flow statement for Walmart's fiscal year, which ended on January 31, 2019, is shown here. All sums are expressed in millions of dollars.

The last line of the cash flow statement, "cash and cash equivalents at end of year," is the same as the first line under current assets on the balance sheet, "cash and cash equivalents." Consolidated net income, which appears as the first number in the cash flow statement, corresponds to the income from continuing operations figure at the bottom of the income statement.

The net change in cash is determined by making adjustments to operating income because the statement of cash flows only counts liquid assets in the form of CCE. The income statement includes depreciation and amortization to accurately depict how assets depreciate over the course of their useful lives. These modifications are inverted for operating cash flows, which only take into account transactions that affect cash.

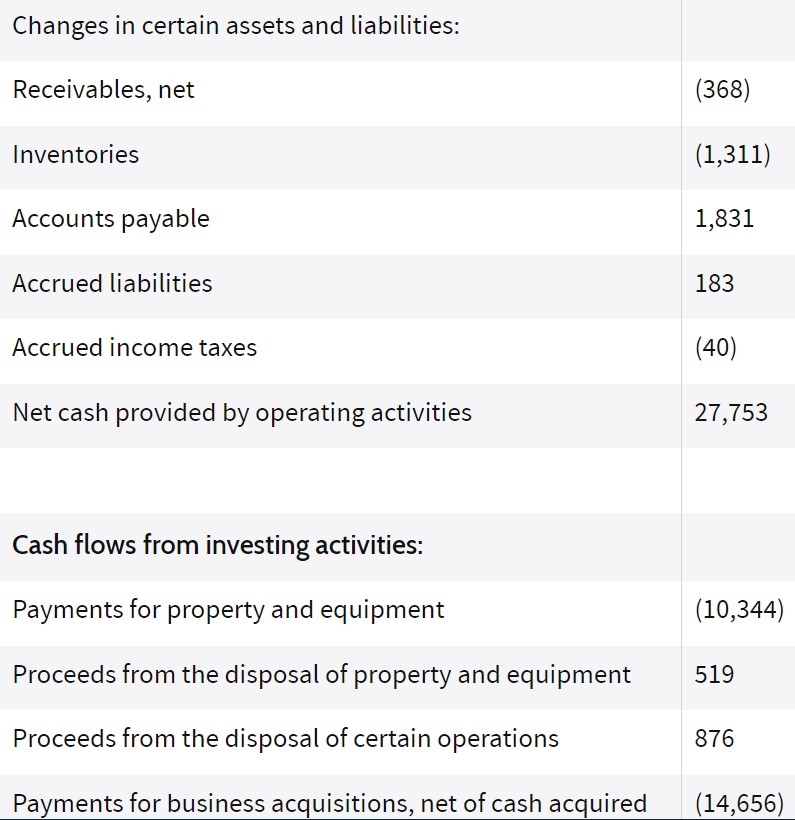

Operating income is also reduced by the net change of non-cash assets like inventories and accounts receivable. Net receivables of $368 million, for instance, are subtracted from operating income. That means that the number of receivables during the previous year increased by $368 million.

The additional revenue from this increase would have been shown in operational income, but by year's end, the cash hadn't been received. To display the net cash impact of sales for the year, the rise in receivables has to be reversed. To calculate cash flow from operations, the same elimination process is used for current liabilities.

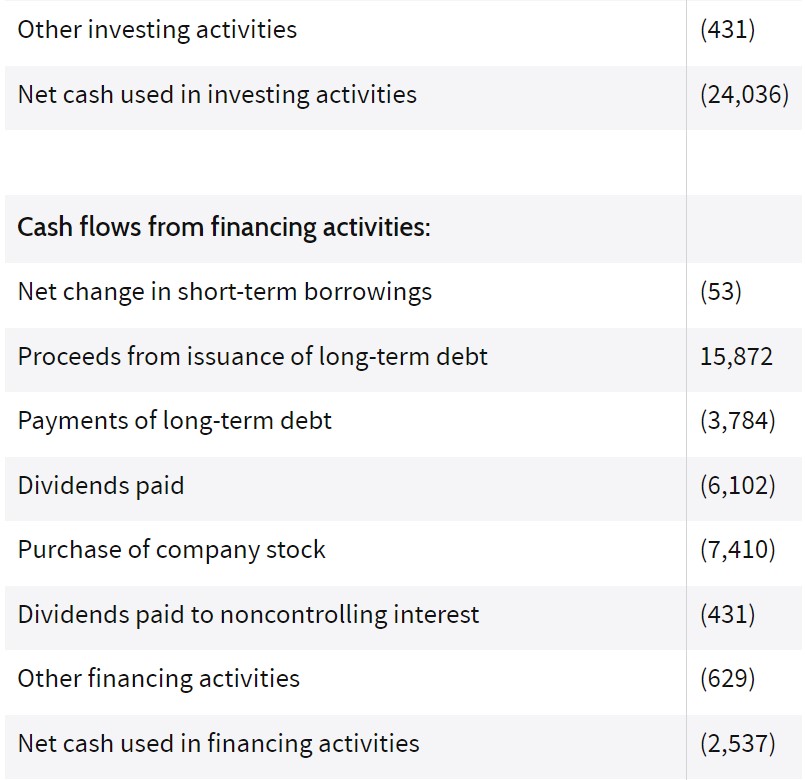

The cash flow from investing activities accounts for expenditures on property, plant, and equipment (PP&E) and purchases of other companies. Cash flow from financing activities includes earnings from issuing long-term debt, paying down debt, and dividends distributed.

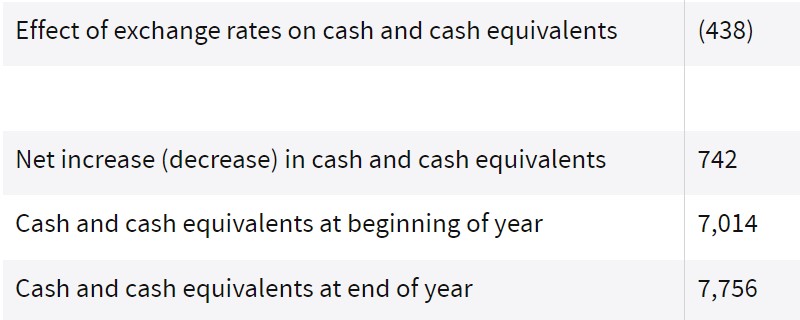

The key finding is a $742 million increase in Walmart's cash flow, which was good. This shows that money has been kept in the company and reserves have been built up to deal with future swings and short-term liabilities.

The money made from selling goods and services is referred to as revenues. When an item is sold on credit or through a subscription payment plan, the money from those sales may not yet have been received and is recorded as accounts receivable. But these don't represent the company's real cash inflows at the time. Both inflows and outflows are tracked by cash flows, which classify them according to their source or purpose.

The money that remains after a corporation pays its operational costs and capital expenditures is known as free cash flow. It is the money that is left over after paying for expenses including rent, taxes, and wages. FCF can be used however the business sees fit.

Knowing how to calculate and evaluate FCF aids a company in managing its cash flow and gives investors knowledge of its finances, enabling them to make wiser investment choices.

FCF is a crucial metric since it reveals how effectively a business generates cash.

The term "cash flow" describes the movement of money. A positive cash flow means that more money is flowing in, whereas a negative cash flow denotes more spending. The latter isn't always a bad thing because it could indicate that you're putting money toward growth. However, if you start to overspend and don’t perform a cash flow analysis, you won't have enough money for a rainy day and won't be able to make payments to your suppliers or lenders. It's critical to manage your cash flow, whether you're a business owner or a homemaker.

Still have some questions about cash flow? Or have you faced any cash flow problems? If so, let's have a look at our FAQ list below – there, you'll definitely find the answers to all of your outstanding issues.

The net balance of money coming into and going out of a business at a particular period is referred to as cash flow.

The price-to-cash flow ratio (P/CF) is a measure of a company's market value and is used to determine whether it is overvalued or undervalued.

A simple cash flow statement is one of the key elements of a company's financial reporting, along with an income statement and a balance sheet. Since 1987, the Financial Accounting Standards Board (FASB) has mandated that companies use a cash flow statement.

Companies should monitor and analyze three forms of cash flow: cash flow from operating activity, cash flow from investment activities, and cash flow from financing activities to assess their liquidity and solvency. A company's cash flow statement will include all three.

© 2024 Lime Trading (CY) Ltd

Lime Trading (CY) Ltd is authorised and regulated by the Cyprus Securities and Exchange Commission in accordance with license No.281/15 issued on 25/09/2015. The "Just2Trade" trademark is owned by LimeTrading (CY) Ltd.

Registration Number: HE 341520

Address: Lime Trading (CY) Ltd

Magnum Business Center, Office 4B, Spyrou Kyprianou Avenue 78

Limassol 3076, Cyprus

Disclaimer:

All promotions, materials and information of this website may have applied conditions. Please contact the Company for further details

Trading on financial markets carries risks. The value of the investments can both increase and decrease and the investors may lose all their investment capital. In case of a leveraged product, the loss may be more than the initial capital invested. Detailed information on risks associated with trading on financial markets can be found in General Terms and Conditions for the Provision of Investment Services..

E-mail: 24_support@just2trade.online