How to Invest in Stocks: A Step-by-Step Guide for Beginners

)

Table of Contents

Understanding Stock Market Fundamentals

Setting Yourself Up for Investment Success

Step-by-Step Guide to Making Your First Stock Investment

Building and Managing a Diversified Portfolio

Long-Term Investment Strategies for Wealth Building

Common Pitfalls to Avoid as a New Investor

Advanced Techniques to Consider as You Gain Experience

How Old Do You Have to Be to Invest in Stocks: Special Considerations

Conclusion and Next Steps

Frequently Asked Questions

The stock market represents one of the most powerful wealth-building platforms available, yet many potential investors delay taking first steps due to uncertainty. Stock investing transforms capital into equity ownership in businesses, generating returns through capital appreciation and dividend income. This guide provides practical strategies bridging the gap between beginner hesitation and confident execution. Whether starting with $500 or $5,000, successful stock trading requires understanding fundamentals, managing risk intelligently, and maintaining disciplined long-term strategies.

Key Takeaways:

- Establish clear goals and assess risk tolerance before investing

- Begin with diversified index funds or blue-chip stocks

- Use dollar-cost averaging for consistent position building

- Maintain 3-6 month emergency fund separate from investments

- Focus on long-term wealth building, not short-term trading

Understanding Stock Market Fundamentals

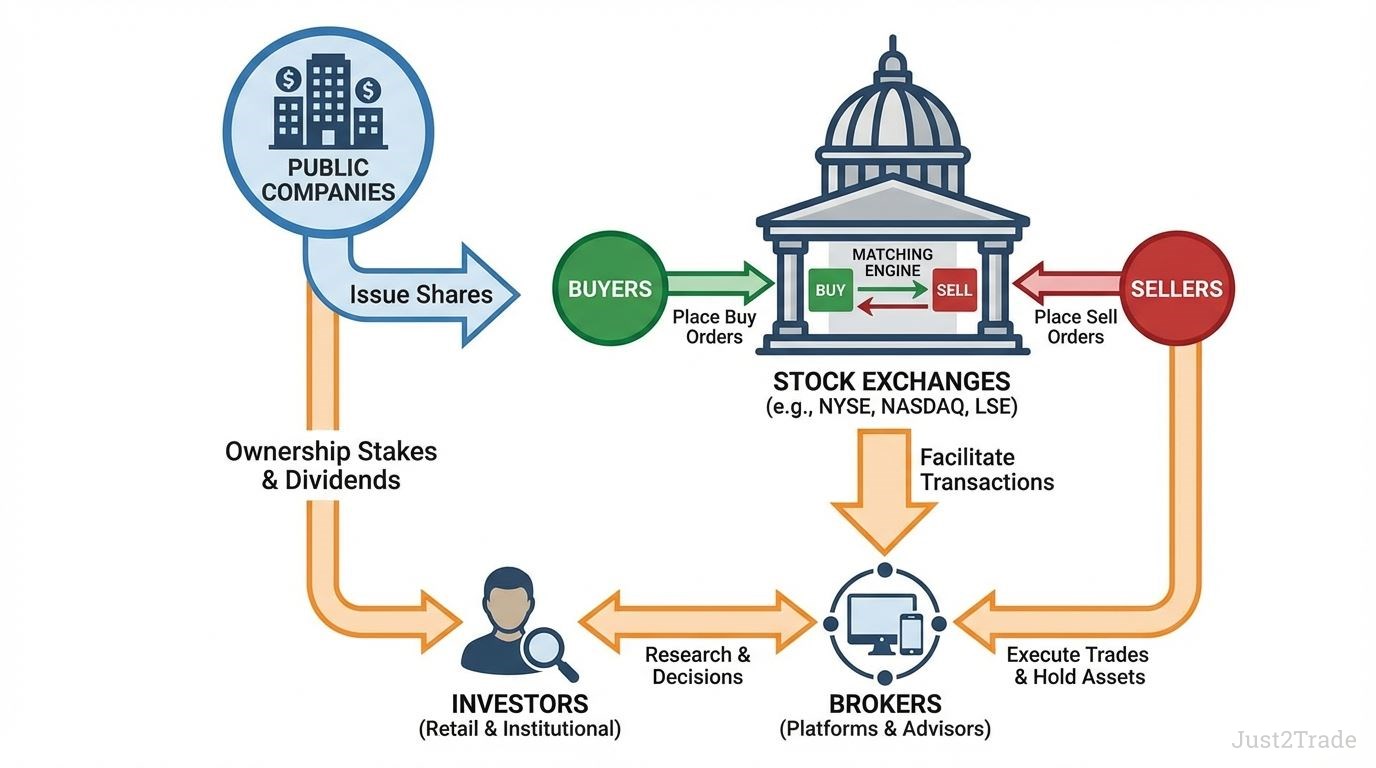

The stock market operates as a regulated marketplace where investors exchange ownership stakes in publicly traded companies. Stock exchanges—including the London Stock Exchange, NYSE, and NASDAQ—connect buyers and sellers through electronic platforms. Common stock represents fractional ownership, entitling shareholders to proportional profit claims and voting rights. Stock market indices like the FTSE 100 or S&P 500 track performance across selected companies, offering benchmarks measuring market health. Understanding how exchanges facilitate transactions, what ownership means, and how prices reflect investor sentiment forms the foundation for confident investing.

)

What Are Stocks and Why Should You Invest in Them?

Common stock represents ownership shares in publicly traded corporations, transforming investors into partial business owners with claims on company assets and earnings. Stock ownership generates returns through capital appreciation when share prices increase, and dividend income when companies distribute earnings. Equities historically outpace inflation and fixed-income securities, delivering average annual returns of 8-10% across decades. Stock investing offers portfolio diversification, liquidity, and tax advantages through preferential capital gains treatment.

Key Benefits of Stock Investing:

- Wealth Building: Compound growth exceeding savings accounts

- Passive Income: Regular dividend payments

- Inflation Protection: Returns outpacing rising costs

- Tax Efficiency: Favorable capital gains rates

- Ownership Rights: Voting power in corporate decisions

How the Stock Market Works

Stock exchanges function as regulated platforms where buyers and sellers execute transactions through standardized procedures. Brokerage platforms provide retail investors with market access. When investors place orders, exchanges match buy and sell requests through algorithms based on supply and demand. The bid-ask spread reflects market liquidity and trading costs. Market orders guarantee immediate fills at current prices, limit orders specify maximum purchase or minimum selling prices, and stop orders trigger automatically at predetermined thresholds.

Stock Market Order Types Comparison:

| Order Type |

Execution Method |

Advantages |

Best Use Cases |

| Market Order |

Fills immediately at current market price |

Guaranteed execution, fast completion |

High-liquidity stocks, urgency to enter/exit |

| Limit Order |

Executes only at specified price or better |

Price control, prevents overpaying |

Volatile stocks, specific entry/exit targets |

| Stop Order |

Triggers market order when price threshold reached |

Automatic loss protection, hands-off management |

Protecting gains, limiting downside risk |

| Stop-Limit Order |

Triggers limit order at specified price after threshold |

Combines stop protection with price control |

Precise exit strategy, volatile conditions |

Capital Gains vs. Dividends: Two Ways Stocks Generate Returns

Common stock generates returns through capital gains from price appreciation and dividend income from profit distributions. Capital gains occur when share prices increase above purchase costs. Dividends represent quarterly or annual cash payments to shareholders, providing passive income without requiring share sales. Total return combines both—a stock rising from $50 to $60 (20% gain) while paying $2 dividends (4% yield) delivers 24% total return.

Total Return Example:

- Purchase: $50/share → Current: $60/share (20% gain)

- Annual Dividend: $2/share (4% yield)

- Total Return: 24%

Setting Yourself Up for Investment Success

Successful investment begins with establishing a solid financial foundation. Investor readiness requires completing essential prerequisites: securing emergency funds covering 3-6 months expenses, eliminating high-interest debt, and defining clear financial goals with specific timeframes. Investment planning transforms vague aspirations into actionable strategies aligned with risk tolerance. This preparation determines whether market volatility triggers panic selling or presents strategic opportunities.

Financial Prerequisites Before Investing:

- Emergency Fund: 3-6 months expenses in accessible savings

- High-Interest Debt Eliminated: Credit cards and personal loans paid off

- Investment Goals Defined: Specific objectives with amounts and timeframes

- Risk Tolerance Assessed: Honest evaluation of comfort with portfolio fluctuations

- Investment Budget Determined: Monthly contribution amount maintaining financial stability

Determining Your Investment Goals and Risk Tolerance

Investor success requires aligning strategies with precise financial objectives and realistic risk tolerance. Investment goals should specify exact amounts, timeframes, and purposes—accumulating $50,000 for property deposits within seven years or building $500,000 retirement portfolios over thirty years. Risk tolerance reflects capacity to withstand portfolio volatility without panic selling. Investment management principles connect time horizons to appropriate strategies: aggressive growth suits investors with 20+ year timeframes, while capital preservation benefits those needing funds within five years.

Risk Tolerance Self-Assessment:

Answer these questions to determine your risk profile:

- Time Horizon: When will you need this money? (15+ years = High risk / 3-7 years = Moderate / Under 3 years = Low risk)

- Market Downturn: If your portfolio drops 20%, would you buy more, hold steady, or sell? (Buy = High risk / Hold = Moderate / Sell = Low risk)

- Income Stability: How secure is your employment? (Very stable = High risk / Moderate = Moderate risk / Uncertain = Low risk)

Creating an Investment Budget You Can Stick With

Investment success depends on consistent capital allocation that maintains financial stability rather than aggressive contributions that strain monthly budgets. Dollar cost averaging—investing fixed amounts at regular intervals regardless of market conditions—builds discipline while reducing market timing risk through automatic position building. Recommended allocation percentages scale with career progression: 10-15% of gross income during early career establishment, 15-20% during mid-career earnings growth, and 20%+ approaching peak earning years. This systematic approach transforms investing from sporadic large deposits into sustainable wealth-building habits.

Budgeting Tips for New Investors:

- Start with manageable amounts ($50-$100 monthly) rather than delaying until accumulating larger sums

- Automate transfers on payday to prioritize investing before discretionary spending

- Increase contributions by 1-2% annually as income rises without impacting lifestyle

- Treat investment contributions as non-negotiable fixed expenses like rent or utilities

- Use windfalls (bonuses, tax refunds) to boost portfolio without adjusting monthly budget

Understanding Different Account Types for Stock Investing

Brokerage platforms offer multiple account types with distinct tax treatments and withdrawal rules that significantly impact investment returns. Tax-advantaged retirement accounts—including 401(k)s, Traditional IRAs, and Roth IRAs—provide tax deductions or tax-free growth in exchange for restricted access until age 59½. Taxable brokerage accounts offer complete flexibility for withdrawals but subject gains to capital gains taxation. Investment account selection should prioritize maximizing employer 401(k) matches (immediate 50-100% returns), then funding Roth IRAs for tax-free growth ($6,500 annual limit), and finally utilizing taxable accounts for additional capital deployment and shorter-term goals requiring liquidity.

Account Types Comparison:

| Account Type |

Tax Treatment |

Contribution Limit |

Withdrawal Rules |

Best Use |

| 401(k) |

Tax-deductible contributions; taxed on withdrawal |

$22,500/year |

Penalty before 59½ |

Employer match; long-term retirement |

| Roth IRA |

After-tax contributions; tax-free withdrawals |

$6,500/year |

Contributions accessible; gains restricted |

Tax-free retirement growth |

| Traditional IRA |

Tax-deductible contributions; taxed on withdrawal |

$6,500/year |

Penalty before 59½ |

Tax deduction; retirement savings |

| Taxable Brokerage |

Capital gains tax on profits |

No limit |

Unrestricted access |

Flexibility; pre-retirement goals |

Step-by-Step Guide to Making Your First Stock Investment

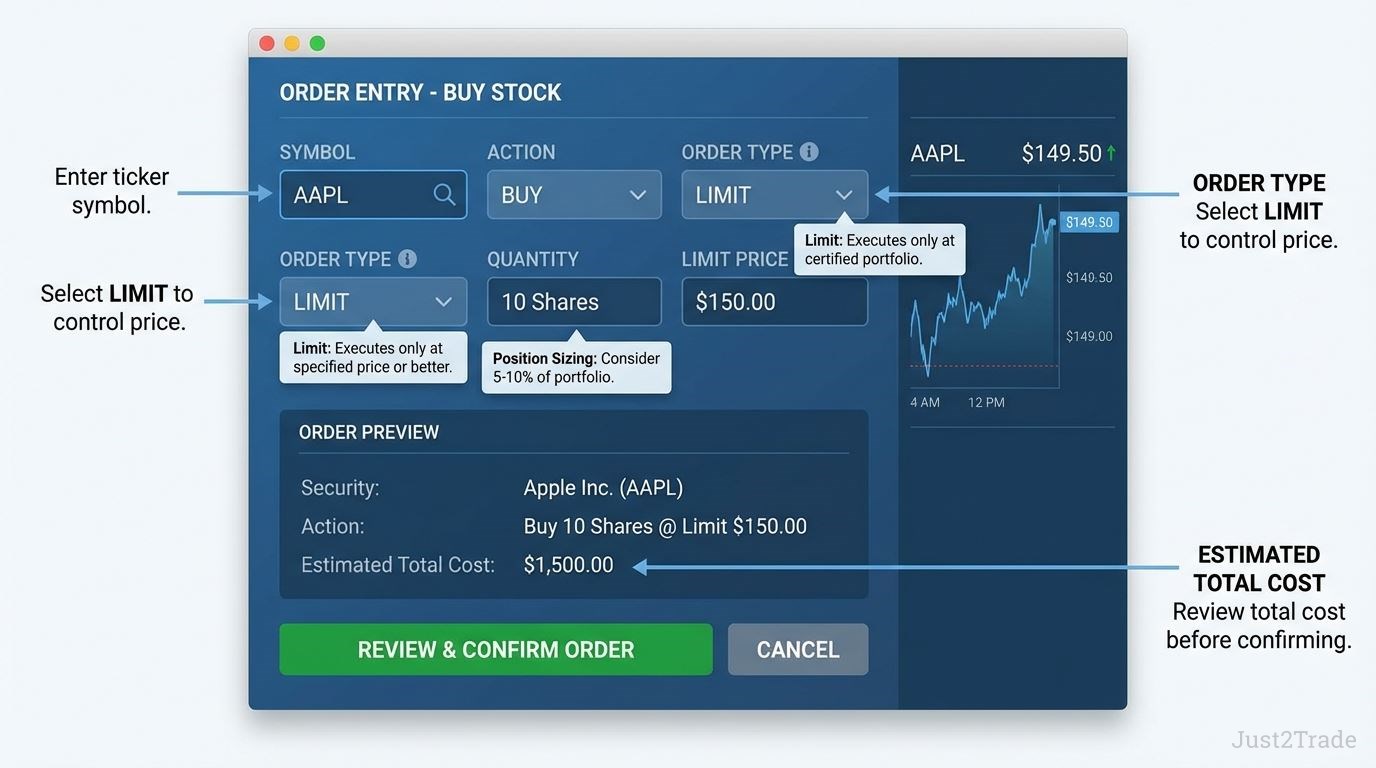

Executing a first stock purchase requires systematic procedures reducing anxiety and preventing mistakes. Select a brokerage platform prioritizing user-friendly interfaces, commission-free trading, and regulatory compliance (Fidelity, Charles Schwab, Vanguard). Open accounts through identity verification and bank linking, with funding clearing in 2-3 days. Research established companies with consistent profitability and reasonable valuations before purchase. Execute trades by selecting ticker symbols, choosing limit orders for price control, and confirming transactions. Start with fractional shares or index funds to gain experience without substantial risk.

First Investment Process:

- Select brokerage platform and verify regulatory registration

- Open account with personal details and bank linking

- Fund account via bank transfer (2-3 days settlement)

- Research established companies with consistent earnings

- Place limit order with appropriate position size (5-10% portfolio)

- Confirm trade and monitor weekly (not daily)

Choosing the Right Brokerage Account

Select brokers offering commission-free trading, user-friendly platforms, educational resources, and regulatory compliance. Major platforms include Fidelity (excellent research tools), Charles Schwab (strong customer service), Vanguard (low-cost index funds), and E-Trade (advanced charting). Beginners benefit from fractional share access and paper trading simulators.

How to Invest in Shares: Researching and Selecting Your First Stocks

Research established companies with profitable track records, reasonable valuations, and understandable business models. Examine P/E ratios below industry averages, revenue growth exceeding 5-10% annually, debt-to-equity under 1.0, and dividend yields indicating stability. Focus on blue-chip stocks with market caps exceeding $10 billion demonstrating resilient business models.

Key Metrics:

- P/E Ratio (compare to peers), Dividend Yield (2-4%), Debt-to-Equity (<1.0), Revenue Growth (5-10%+)

Executing Your First Trade

Enter ticker symbols, select limit orders specifying maximum prices, and avoid market opens/closes when volatility peaks. Position sizing should limit first trades to 5-10% of portfolio value. Review order previews showing total costs before confirming. Trade confirmations arrive via email documenting price, quantity, and settlement date.

)

Building and Managing a Diversified Portfolio

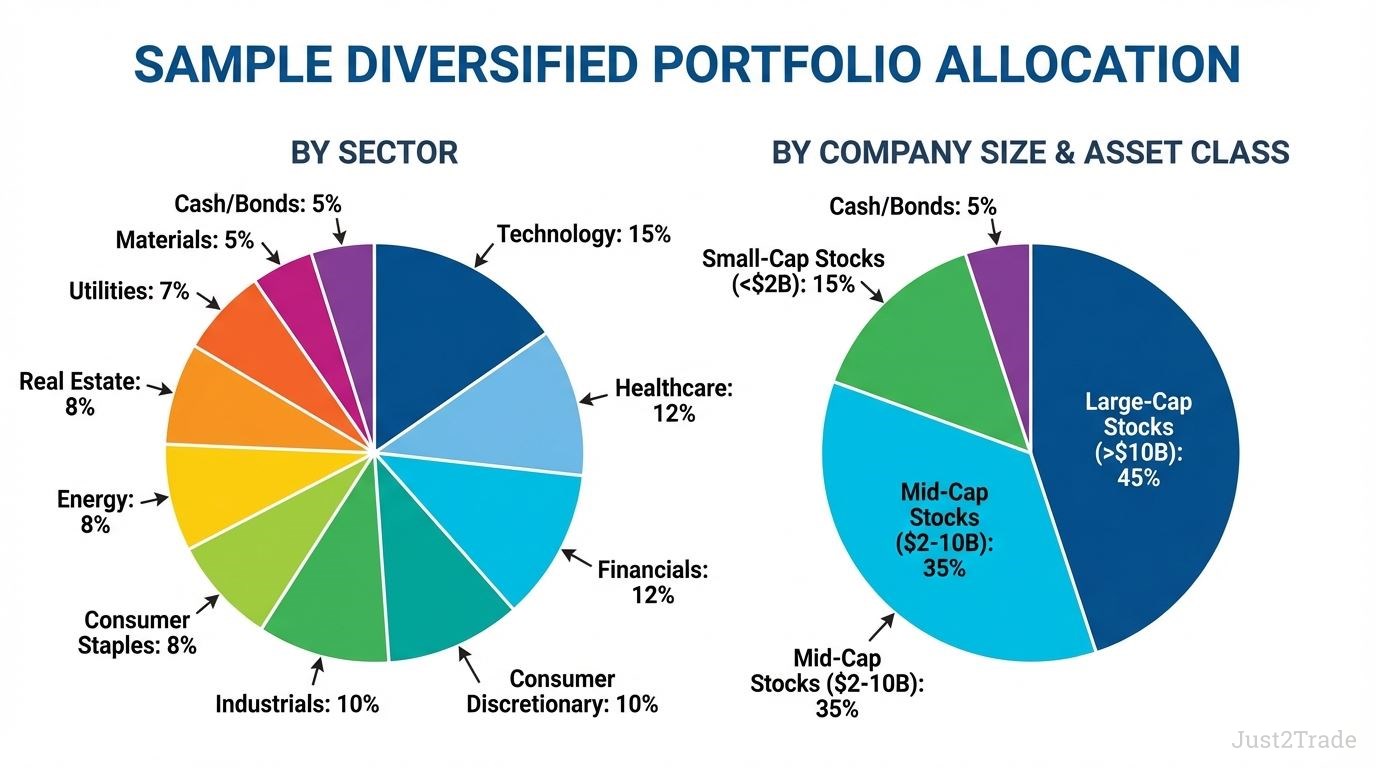

Portfolio diversification reduces risk by distributing investments across multiple securities, sectors, and asset classes rather than concentrating capital in individual positions. Investment funds—particularly index funds and ETFs—provide instant diversification by holding hundreds or thousands of stocks in single securities, making them ideal foundation holdings for beginners. Investment management principles recommend allocating portfolios across 8-10 distinct sectors including technology, healthcare, financials, consumer goods, and industrials, with each sector representing 10-15% of total holdings to prevent concentration risk. Common stock diversification extends beyond sectors to include company size distribution: 40-50% large-cap stocks (market capitalization exceeding $10 billion), 30-40% mid-cap ($2-10 billion), and 10-20% small-cap (under $2 billion). Stock market indices like the S&P 500 or FTSE 100 serve as diversification benchmarks, with well-diversified portfolios containing 15-25 individual positions across multiple sectors demonstrating resilience during market downturns.

Sample Diversified Portfolio Allocation:

By Sector:

- Technology: 15%

- Healthcare: 12%

- Financials: 12%

- Consumer Discretionary: 10%

- Industrials: 10%

- Consumer Staples: 8%

- Energy: 8%

- Real Estate: 8%

- Utilities: 7%

- Materials: 5%

- Cash/Bonds: 5%

By Company Size:

- Large-Cap Stocks (>$10B): 45%

- Mid-Cap Stocks ($2-10B): 35%

- Small-Cap Stocks (<$2B): 15%

- Cash/Bonds: 5%

)

How to Invest in Stocks for Beginners with Little Money: Diversification Strategies

Investment funds democratize diversification for limited budgets, with index ETFs requiring as little as $100-500 for positions holding hundreds of companies. Common stock fractional share ownership eliminates barriers to expensive stocks—purchasing 0.1 shares of a $1,000 stock costs just $100, enabling portfolio diversity regardless of individual share prices. Dollar cost averaging transforms limited capital into systematic wealth building through consistent small contributions: investing $100-200 monthly into broad market index funds creates diversified exposure without timing market entry points. Low-cost index ETFs tracking S&P 500 or total market indices charge expense ratios under 0.10% annually, preserving returns while providing instant diversification across sectors and company sizes.

Diversification Options for Limited Capital:

- Index ETFs: Broad market exposure from $100 minimum (e.g., VOO, VTI, SCHB)

- Fractional Shares: Purchase partial shares of expensive stocks through major brokers

- Dividend Reinvestment Plans (DRIPs): Automatically reinvest dividends to compound holdings

- Target-Date Funds: Age-appropriate diversification from $1,000 minimum

- Robo-Advisors: Automated portfolio management starting at $500 with 0.25% fees

- Micro-Investing Apps: Round-up spare change investments building diversified portfolios

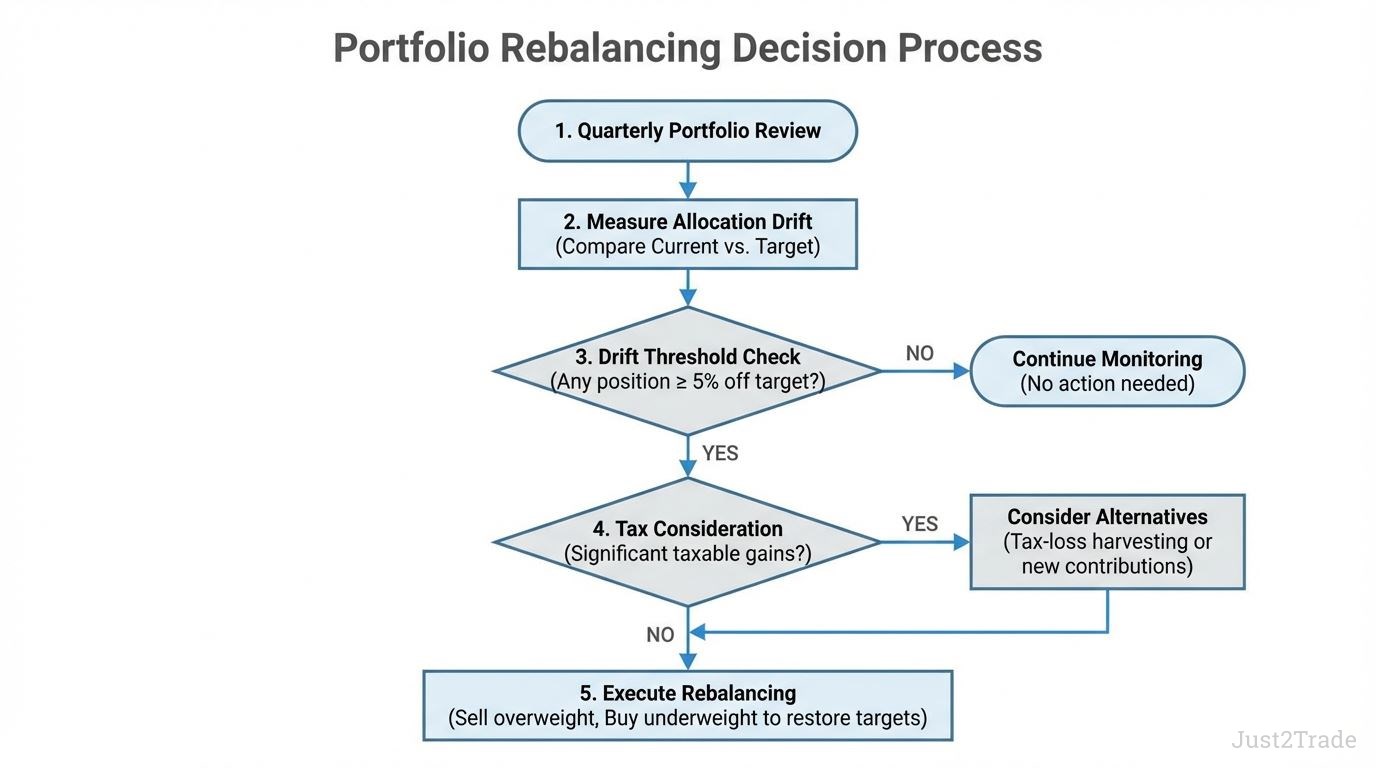

When and How to Rebalance Your Portfolio

Investment management discipline requires periodic portfolio rebalancing to maintain target allocations as common stock positions grow disproportionately through market movements. Rebalancing triggers activate when any position drifts 5+ percentage points from target allocation—a technology sector growing from 15% to 21% target warrants rebalancing. Quarterly portfolio reviews identify allocation drift, with actual rebalancing executed annually or when thresholds breach, avoiding excessive transaction activity and tax consequences. The rebalancing process involves selling overweighted positions that exceeded targets, then purchasing underweighted sectors or assets that fell below allocations, effectively enforcing "buy low, sell high" discipline through systematic rules rather than emotional decisions. This risk management technique prevents concentration risk while capturing gains from outperforming positions.

Portfolio Rebalancing Decision Flowchart:

- Review Frequency: Quarterly portfolio allocation check

- Measure Drift: Compare current allocation to target percentages

-

Threshold Check: Has any position moved 5+ percentage points from target?

- NO → Continue monitoring, no action needed

- YES → Proceed to step 4

-

Tax Consideration: Will rebalancing create significant taxable gains?

- YES → Consider tax-loss harvesting or use new contributions to rebalance

- NO → Proceed to step 5

- Execute Rebalancing: Sell overweighted positions, buy underweighted positions to restore targets

)

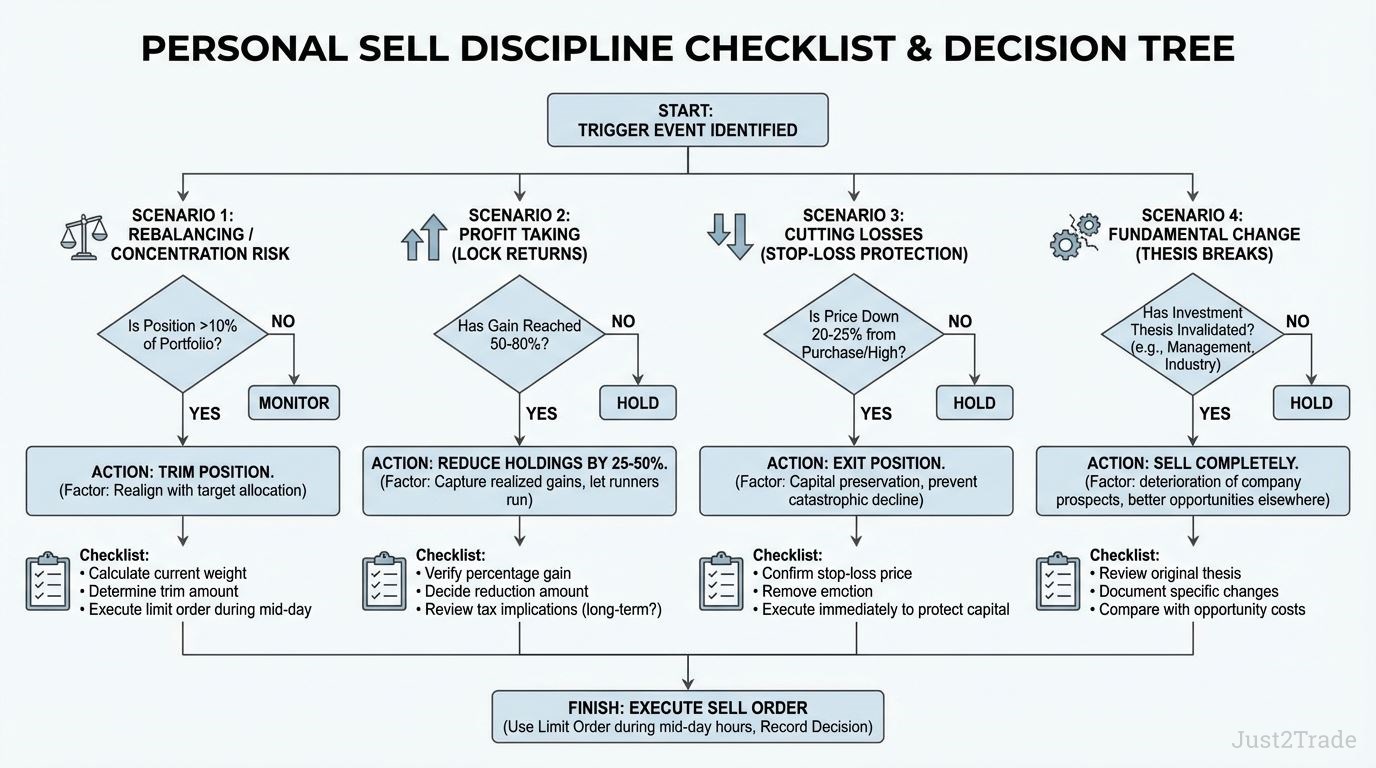

The Art of Selling: When to Exit Your Investments

Stock trader discipline requires predetermined exit criteria preventing emotional decisions during market volatility. Common stock selling triggers include positions exceeding 10% of portfolio value (concentration risk), fundamental thesis invalidation when company prospects deteriorate materially, and superior opportunity identification requiring capital reallocation. Trading strategy frameworks implement 20-25% stop-losses protecting against catastrophic declines while allowing normal volatility, and establish profit-taking rules like trimming positions after 50-80% gains to capture returns. Exit execution timing mirrors entry strategy—using limit orders during mid-day trading hours to control prices. The most challenging selling decision involves declining positions where hope for recovery competes against evidence suggesting permanent impairment; disciplined portfolio management prioritizes capital preservation over ego protection.

Selling Decision Framework:

- Concentration Management: Trim positions exceeding 10% of total portfolio value

- Stop-Loss Protection: Exit positions declining 20-25% from purchase price or recent highs

- Profit-Taking Rules: Reduce holdings by 25-50% after 50-80% gains to lock returns

- Fundamental Change: Sell when investment thesis breaks (management changes, competitive threats, industry disruption)

- Opportunity Cost: Exit underperforming positions when superior alternatives emerge

- Tax Considerations: Time sales to optimize long-term capital gains treatment when possible

)

Long-Term Investment Strategies for Wealth Building

Buy and hold strategy leverages compound growth as the primary wealth-building mechanism, with extended time horizons enabling returns that significantly outpace short-term trading. Value investing guides stock selection by identifying undervalued companies trading below intrinsic worth—seeking low price-to-earnings ratios, strong balance sheets, and sustainable competitive advantages. Investment compounding generates exponential growth: $10,000 invested at 10% annually becomes $67,275 after 20 years and $174,494 after 30 years without additional contributions. Common stock portfolios held through complete market cycles including 2008 and 2020 downturns delivered positive returns by maintaining positions during temporary declines. Patient investors benefit from avoiding market timing mistakes, reducing transaction costs and taxes, and capturing full bull market recoveries.

Compound Growth Illustration:

| Years Invested |

Initial $10,000 @ 8% Annual Return |

Initial $10,000 @ 10% Annual Return |

| 5 years |

$14,693 |

$16,105 |

| 10 years |

$21,589 |

$25,937 |

| 20 years |

$46,610 |

$67,275 |

| 30 years |

$100,627 |

$174,494 |

How to Invest in Dividend Stocks for Passive Income

Common stock dividend investing focuses on companies paying consistent cash distributions to shareholders, creating passive income streams alongside capital appreciation potential. Investment criteria for quality dividend stocks include yields between 3-6% (higher often signals distress), 10+ year dividend payment histories demonstrating reliability, payout ratios below 70% ensuring sustainability, and consistent earnings growth supporting future increases. Dividend reinvestment plans (DRIPs) automatically purchase additional shares using dividend payments, compounding returns through accumulating ownership without transaction fees. Income-focused portfolios typically allocate 30-50% to dividend-paying stocks across sectors, generating monthly cash flow while maintaining growth exposure through remaining holdings.

Quality Dividend Stocks vs. Dividend Traps:

| Characteristic |

Quality Dividend Stock |

Dividend Trap (Avoid) |

| Dividend Yield |

3–6% sustainable range |

8%+ unsustainably high |

| Payment History |

10+ years consecutive payments |

Inconsistent or recently initiated |

| Payout Ratio |

40–70% of earnings |

Above 80% or exceeds earnings |

| Earnings Trend |

Growing or stable profits |

Declining revenue/earnings |

| Debt Levels |

Manageable debt-to-equity < 1.0 |

High leverage risk |

| Industry Position |

Market leader with advantages |

Declining industry or market share |

Value Investing vs. Growth Investing

Value investing focuses on undervalued stocks trading below intrinsic worth, seeking companies with low price-to-book ratios, modest P/E multiples, and strong fundamentals offering safety margins. Growth investing targets companies expanding revenue and earnings rapidly, accepting higher valuations for anticipated future performance in sectors like technology and healthcare. Investment strategy selection depends on market conditions—value stocks typically outperform during economic recoveries and rising interest rates, while growth stocks excel during expansionary periods with low rates. Balanced portfolios often blend both approaches: 50-70% value positions providing stability and dividends, 30-50% growth holdings capturing innovation-driven appreciation. Undervalued stock identification requires patience as market recognition may take years, whereas growth investing demands conviction in disruptive business models despite near-term unprofitability.

Value vs. Growth Investing Comparison:

| Aspect |

Value Investing |

Growth Investing |

| Target Companies |

Established, undervalued firms |

High-growth, innovative companies |

| Key Metrics |

Low P/E, P/B ratios; high dividend yield |

High revenue growth; expanding margins |

| Risk Profile |

Lower volatility; margin of safety |

Higher volatility; execution risk |

| Time Horizon |

3–7 years for revaluation |

5–10+ years for growth realization |

| Famous Practitioners |

Warren Buffett, Benjamin Graham |

Peter Lynch, Cathie Wood |

| Market Conditions |

Outperforms in recoveries, rising rates |

Excels in expansions, low-rate environments |

Common Pitfalls to Avoid as a New Investor

Investor mistakes typically stem from emotional decisions, inadequate research, and poor risk management. Stock trader behavioral traps include buying on hype without fundamental analysis, panic selling during downturns, and holding losing positions excessively long hoping for recovery. Investment discipline requires systematic processes: research checklists before purchases, predetermined selling rules, and position sizing limits capping holdings at 5-10% of portfolio value. Common beginner errors include market timing attempts, overtrading generating excessive fees, concentration in familiar sectors lacking diversification, and investing before establishing emergency funds. Learning from mistakes separates successful long-term investors from those abandoning markets after initial setbacks.

Common Investment Mistakes and Prevention:

- Buying on Hype: Investing based on social media tips without research → Solution: Complete fundamental analysis checklist before any purchase

- Panic Selling: Exiting positions during market downturns from fear → Solution: Maintain 6-month emergency fund; focus on long-term goals during volatility

- Holding Losers: Refusing to sell declining stocks hoping for recovery → Solution: Implement 20-25% stop-loss rules; reassess thesis quarterly

- Market Timing: Attempting to predict short-term tops and bottoms → Solution: Use dollar-cost averaging; ignore short-term predictions

- Overconcentration: Allocating 20%+ portfolio to single stock → Solution: Limit individual positions to 5-10% maximum

- Chasing Returns: Buying last year's winners at peak valuations → Solution: Focus on forward prospects, not past performance

- Ignoring Fees: Underestimating transaction costs and expense ratios → Solution: Prioritize low-cost index funds; minimize trading frequency

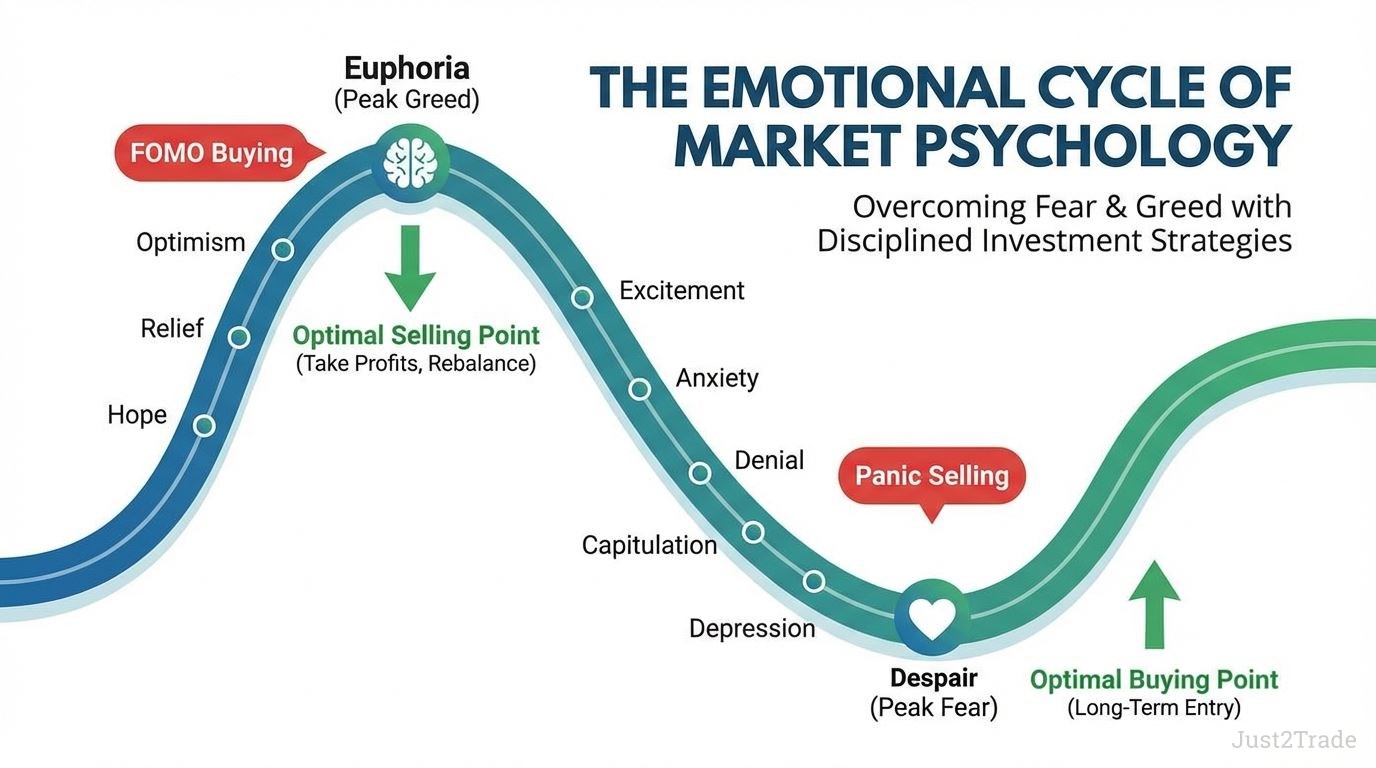

Emotional Decision-Making and How to Overcome It

Investor psychology significantly impacts returns, with fear and greed driving suboptimal decisions during market extremes. Stock trader emotional discipline requires structured frameworks: maintaining written investment theses for each position, establishing predetermined entry/exit rules eliminating real-time emotional choices, and limiting portfolio reviews to weekly frequency reducing volatility-triggered anxiety. Common emotional patterns include panic selling during drops, FOMO buying near peaks, and excessive trading from boredom. Successful management involves accepting volatility as normal, focusing on long-term goals during downturns, and recognizing that missing short-term gains matters less than avoiding catastrophic mistakes.

Emotional Discipline Techniques:

- Document written investment thesis for every position before purchase

- Set calendar reminders for quarterly reviews; avoid daily price checking

- Establish "cooling-off period" of 24-48 hours before emotional sells

- Maintain pre-committed rebalancing schedule regardless of market sentiment

- Focus on portfolio progress toward goals, not daily dollar fluctuations

)

High-Risk Investments to Avoid as a Beginner

Investment vehicles requiring advanced knowledge should be avoided until solid foundations exist. Trading strategy complexity in derivatives like options involves time decay, leverage, and pricing models beyond beginner comprehension. Penny stocks under $5 face fraud risk, extreme illiquidity, and manipulation. Margin trading amplifies losses through borrowed capital, potentially triggering liquidation. Day trading shows 95%+ failure rates due to costs, emotional pressure, and institutional advantages. Build competency through index funds and blue-chips for 2-3 years before attempting higher-risk strategies.

High-Risk Investments to Avoid as Beginner:

- Penny Stocks: Companies under $5/share often lack transparency, face manipulation, suffer extreme illiquidity

- Options Trading: Complex derivatives with time decay; requires understanding Greeks, volatility, expiration mechanics

- Margin Trading: Borrowed capital amplifies losses; can lose more than initial investment during crashes

- Day Trading: 95%+ failure rate; transaction costs and emotional stress overwhelm most participants

- Leveraged ETFs: 2x-3x daily multipliers decay over time; unsuitable for holding periods beyond single day

Advanced Techniques to Consider as You Gain Experience

Investment management sophistication develops after mastering fundamentals through 2-3 years of consistent practice. Advanced techniques for experienced practitioners include tax-loss harvesting offsetting capital gains, covered calls generating income from holdings, sector rotation capitalizing on economic cycles, and strategic asset location optimizing tax efficiency. Investment evolution follows predictable progression: beginning with index funds and buy-and-hold, advancing to individual stock selection, then incorporating sophisticated techniques like options strategies. Stock trader skill development requires accumulated experience recognizing patterns, managing emotions, and understanding market dynamics textbooks cannot teach. Attempting advanced strategies prematurely risks capital destruction—options losses from misunderstood time decay, tax inefficiency from poor account placement, or overtrading from false confidence.

Investor Progression Roadmap:

Beginner (Year 0-1):

- Index funds and ETFs

- Buy-and-hold strategy

- Basic diversification

- Emergency fund establishment

Intermediate (Year 1-3):

- Individual stock selection

- Dividend investing

- Sector allocation

- Position sizing rules

Advanced (Year 3+):

- Tax-loss harvesting

- Options for income

- Sector rotation timing

- Multi-account tax optimization

Tax-Efficient Investing Approaches

Investment management tax optimization significantly impacts after-tax returns through strategic account placement and timing decisions. Growth stocks benefit from long-term capital gains rates (0-20%) versus ordinary income rates (up to 37%) when held beyond one year, while dividend-paying stocks perform better in tax-advantaged accounts avoiding annual income taxation. Tax-loss harvesting captures portfolio losses to offset realized gains, reducing annual tax bills by $3,000+ through strategic selling and replacement with similar securities. Investment tax awareness requires reviewing potential tax impacts before rebalancing—selling positions with substantial gains triggers immediate taxation, whereas holding or harvesting offsetting losses optimizes outcomes. Account placement strategy locates high-dividend REITs and bonds in tax-deferred accounts, growth stocks in taxable accounts benefiting from preferential long-term rates, and municipal bonds in taxable accounts for tax-free income.

Tax-Efficient Asset Placement Guide:

| Asset Type |

Optimal Account |

Tax Reasoning |

| High-Growth Stocks |

Taxable |

Long-term capital gains taxed at 0–20% |

| Dividend Stocks / REITs |

Tax-Advantaged |

Avoids annual ordinary income tax on distributions |

| Bonds / Fixed Income |

Tax-Advantaged |

Interest taxed as ordinary income up to 37% |

| Municipal Bonds |

Taxable |

Interest already tax-free at federal level |

| Index Funds (Low Turnover) |

Either |

Naturally tax-efficient in both account types |

Tax Implications of Stock Investing

Investment taxation varies dramatically based on holding periods and activity type, significantly impacting net returns. Common stock capital gains face ordinary income taxation (10-37%) when held under one year, versus preferential long-term rates (0-20%) for holdings exceeding 12 months—a $10,000 gain costs $3,700 short-term versus $2,000 long-term for high earners. Qualified dividends from US corporations held 60+ days receive preferential rates matching long-term gains, while non-qualified dividends face ordinary income taxation. Tax management requires maintaining detailed transaction records documenting purchase dates, costs, and holding periods for accurate reporting. Strategic approaches include deferring gains realization until qualifying for long-term treatment, harvesting losses before year-end to offset gains, and collaborating with tax professionals for optimization strategies.

Investment Tax Rate Comparison:

| Activity Type |

Holding Period |

Tax Rate |

Example on $10,000 Gain |

| Short-Term Capital Gains |

Under 1 year |

10–37% (ordinary income) |

$1,000–$3,700 |

| Long-Term Capital Gains |

Over 1 year |

0–20% (preferential) |

$0–$2,000 |

| Qualified Dividends |

60+ days holding |

0–20% (preferential) |

$0–$2,000 |

| Non-Qualified Dividends |

Any period |

10–37% (ordinary income) |

$1,000–$3,700 |

Year-End Tax Planning Checklist:

- Review unrealized gains/losses across portfolio (October-November)

- Harvest losses to offset realized gains before December 31

- Consider deferring additional gain realization until January if possible

- Verify qualified dividend holding period requirements (60+ days)

- Document all transactions with dates, amounts, cost basis for tax filing

How Old Do You Have to Be to Invest in Stocks: Special Considerations

Stock market participation requires age 18 for direct account ownership in most jurisdictions, though minors access equity ownership through custodial accounts managed by adults. Investor options for young people include UGMA (Uniform Gifts to Minors Act) and UTMA (Uniform Transfers to Minors Act) accounts enabling parents or guardians to invest on behalf of minors, with assets transferring to the child at legal age (18-21 depending on state). Investment education ideally begins during high school years through paper trading and small custodial positions building practical experience before independent account management. Early investing provides compound growth advantages—$1,000 invested at age 15 becomes $45,000+ by retirement through 50 years of 8% returns, demonstrating why starting young maximizes wealth accumulation despite limited initial capital.

Investment Account Options by Age:

- Under 18: Custodial accounts (UGMA/UTMA) managed by parent/guardian; assets transfer at legal age

- Under 18: 529 Education Savings Plans for college expenses; tax-advantaged growth for education

- Ages 13-17: Teen brokerage accounts (offered by select brokers with parental oversight features)

- Age 18+: Standard individual brokerage accounts; full independent trading authority

- Age 18+: IRA accounts (Traditional/Roth) if earning income; contribution limited to earned income amount

Conclusion and Next Steps

Investment success requires consistent application of fundamental principles: establishing financial foundations, investing regularly through dollar-cost averaging, maintaining long-term perspectives, managing emotions through predetermined rules, and pursuing continuous education. Stock market participation offers wealth-building potential, with disciplined approaches compounding modest contributions into substantial portfolios. Starting small matters less than starting now—compound growth rewards early action.

Next Steps:

- Open brokerage account (Fidelity, Charles Schwab, Vanguard)

- Make first investment in broad index fund (VTI, VOO)

- Establish automatic monthly contributions

- Review portfolio quarterly; avoid daily price checking

FAQ

-

How do I start investing in stocks as a beginner?

Establish a 3-6 month emergency fund and eliminate high-interest debt. Open a brokerage account with platforms like Fidelity or Charles Schwab. Start with index funds or ETFs, investing $100-500 monthly through dollar-cost averaging.

-

How much money do I need to start investing in stocks?

Most brokers require no minimum deposit—start with $1 through fractional shares. However, $500-1,000 provides meaningful diversification. Prioritize consistent monthly contributions over large initial deposits for compound growth benefits.

-

What's the difference between investing in individual stocks and funds?

Individual stocks offer higher potential returns but concentrated risk requiring extensive research. Funds (ETFs, mutual funds) hold hundreds of stocks, providing instant diversification and lower research requirements. Beginners typically start with funds.

-

How do I choose a broker for stock investing?

Select brokers offering commission-free trading, user-friendly platforms, educational resources, and regulatory compliance (FCA, SEC). Compare Fidelity, Charles Schwab, Vanguard, and E-Trade for features like fractional shares and research tools.

-

What are the risks of investing in stocks?

Stock volatility creates short-term losses—portfolios commonly decline 20-30% during corrections. Individual stocks face bankruptcy, management failures, and competitive disruption. Market timing mistakes and inadequate diversification amplify losses. However, long-term diversified portfolios historically recover.

-

How can I invest in stocks with little money?

Use fractional shares from $1, enabling diversification across expensive stocks. Choose low-cost index ETFs (VOO, VTI) from $100-200. Implement dollar-cost averaging with $50-100 monthly contributions. Commission-free trading eliminates transaction costs.

-

How do I build a diversified stock portfolio?

Allocate across 8-10 sectors with 10-15% maximum per sector. Distribute by company size: 40-50% large-cap, 30-40% mid-cap, 10-20% small-cap. Include 15-25 positions or use index funds. Rebalance quarterly when positions drift 5+ points.

-

How do stocks make money for investors?

Stocks generate returns through capital appreciation when prices increase, and dividend income from quarterly cash payments. Total return combines both—a stock rising $10 (20%) while paying $2 dividends (4%) delivers 24% return.

-

What investment strategies work best for beginners?

Buy-and-hold emphasizing diversified index funds or blue-chips minimizes costs and emotional decisions. Dollar-cost averaging reduces timing risk. Value investing provides safety margins. Avoid day trading, options, margin, and speculative investments.

-

What are the tax implications of investing in stocks?

Capital gains face ordinary income tax (10-37%) under one year, versus preferential rates (0-20%) over 12 months. Qualified dividends receive preferential treatment. Use tax-advantaged accounts (401k, IRA) and implement tax-loss harvesting before year-end.