News

We provide the latest news from the world of economics and finance

We provide the latest news from the world of economics and finance

Integer Holdings Corporation ITGR has been gaining from its research and product development activities. The optimism led by a solid fourth-quarter 2023 performance and its solid foothold in the broader MedTech space are expected to contribute further. However, volatility in energy markets and dependence on third-party suppliers are a hurdle.

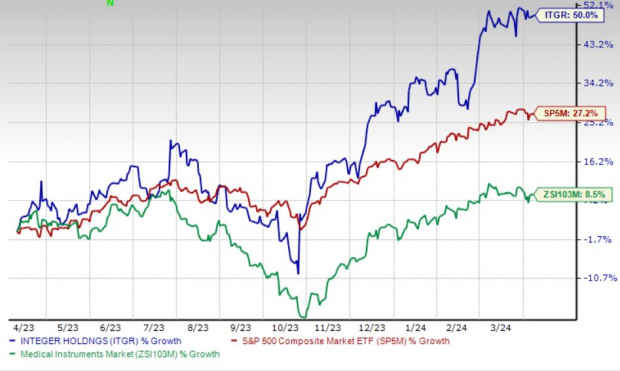

In the past year, this Zacks Rank #3 (Hold) stock has gained 49.9% compared with the 8.5% rise of the industry and the S&P 500’s 27.2% growth.

The renowned medical device outsource manufacturer has a market capitalization of $3.86 billion. The company projects 15% growth for the next five years and expects to maintain its strong performance. Integer Holdings surpassed the Zacks Consensus Estimate in all the trailing four quarters, delivering an earnings surprise of 11.5%, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Research and Product Development: Investors are optimistic about Integer Holdings’ position as a developer and manufacturer of medical devices and components. The company is focused on developing new products, improving and enhancing existing products and expanding the use of its products in new or tangential applications.

In addition to ITGR’s internal technology and capability development efforts aimed at providing its customers with differentiated solutions, the company engages outside research institutions for unique technology projects.

Solid Foothold in the Broader MedTech Space: Investors are optimistic about Integer Holdings’ stable footing in the cardiac, neuromodulation, orthopedics, vascular and advanced surgical markets. Its primary customers include large, multi-national original equipment manufacturers and their affiliated subsidiaries.

ITGR is focused on sales efforts to increase its market penetration in the Cardio & Vascular, Neuromodulation and Non-Medical Electrochem markets. The company is undertaking strategic initiatives to maintain its leadership position in the cardiac rhythm management market.

Strong Q4 Results: Integer Holdings’ robust fourth-quarter 2023 results raise optimism. The company registered year-over-year top-line and bottom-line performances. The Medical segment recorded robust results owing to the strength of its product lines.

Volatility in Energy Markets: Sales of Integer Holdings’ products into the energy market depends upon the condition of the oil and gas industry. Currently, oil and natural gas prices have been subject to significant fluctuation. As a result, the oil and gas exploration and production business are affected by a variety of political and economic factors, including worldwide demand for oil and natural gas and worldwide and domestic supplies of oil and natural gas. Per management, a change in the oil and gas exploration and production industry or a reduction in the exploration and production expenditures of oil and gas companies could cause the company’s energy market revenues to decline.

Dependence on Third-Party Suppliers: Integer Holdings’ business depends on a continuous supply of raw materials, which may be susceptible to fluctuations due to transportation issues, government regulations and price controls, among others. Significant increases in the cost of raw materials, which cannot be recovered through increases in the prices of the company’s products, could adversely affect its operating results.

Integer Holdings is witnessing a positive estimate revision trend for 2024. In the past 90 days, the Zacks Consensus Estimate for earnings has moved 1.7% north to $5.38 per share.

The Zacks Consensus Estimate for the company’s first-quarter 2024 revenues is pegged at $413.3 million, suggesting a 9.1% rise from the year-ago quarter’s reported number.

Some better-ranked stocks in the broader medical space are DaVita Inc. DVA, Cardinal Health, Inc. CAH and Ecolab Inc. ECL.

DaVita, flaunting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 12.1%. DVA’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 35.6%. You can see the complete list of today’s Zacks #1 Rank stocks here.

DaVita’s shares have gained 61.7% compared with the industry’s 16.9% rise in the past year.

Cardinal Health, carrying a Zacks Rank of 2 (Buy) at present, has an estimated long-term growth rate of 14.2%. CAH’s earnings surpassed estimates in each of the trailing four quarters, with the average being 15.6%.

Cardinal Health has gained 37.5% compared with the industry’s 8.9% rise in the past year.

Ecolab, sporting a Zacks Rank of 1 at present, has an estimated long-term growth rate of 13.3%. ECL’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 1.7%.

Ecolab’s shares have rallied 36.7% against the industry’s 5.1% decline in the past year.

Free – 5 Dividend Stocks to Fund Your Retirement

Zacks Investment Research has released a Special Report to help you prepare for retirement with 5 diverse stocks that pay whopping dividends. They cut across property management, upscale outlets, financial institutions, and a couple of strong energy producers.

5 Dividend Stocks to Include in Your Retirement Strategy is packed with unconventional wisdom and insights you won’t get from your neighborhood financial planner.

Download Now – Today It’s FREE >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

© 2024 Lime Trading (CY) Ltd

Lime Trading (CY) Ltd is authorised and regulated by the Cyprus Securities and Exchange Commission in accordance with license No.281/15 issued on 25/09/2015. The "Just2Trade" trademark is owned by LimeTrading (CY) Ltd.

Registration Number: HE 341520

Address: Lime Trading (CY) Ltd

Magnum Business Center, Office 4B, Spyrou Kyprianou Avenue 78

Limassol 3076, Cyprus

Disclaimer:

All promotions, materials and information of this website may have applied conditions. Please contact the Company for further details

Trading on financial markets carries risks. The value of the investments can both increase and decrease and the investors may lose all their investment capital. In case of a leveraged product, the loss may be more than the initial capital invested. Detailed information on risks associated with trading on financial markets can be found in General Terms and Conditions for the Provision of Investment Services..

E-mail: 24_support@just2trade.online