News

We provide the latest news from the world of economics and finance

We provide the latest news from the world of economics and finance

Everyone recognizes Delta Air Lines (NYSE: DAL) as a global transportation giant, ferrying millions of passengers worldwide. While this is true, there's another perspective to consider: Delta is a "plutonomy stock." This term refers to a stock that stands to gain from the growing trend toward wealth imbalances, where the affluent continue to amass wealth.

I'm not advocating for this trend, but I am suggesting that Delta could be a lucrative investment if you believe this trend will persist. Here's why.

First, as Delta's management pointed out during its Investor Day presentation in 2023, "75% of the revenue in our industry is generated from households that have a household income of $100,000 or more, which is the top 40% of consumers in our country."

Given that Delta is not a budget airline and strategically focuses on the premium end, it stands to reason that it will consistently generate revenue from high-end customers, providing a stable investment opportunity.

Second, Delta is growing, and intends to grow, its higher-margin Premium and Loyalty & Other revenue more than its Main cabin revenue. The chart shows that, despite the distortion created by the lockdowns, Delta is growing its higher-margin revenue much more than its Main cabin revenue.

| Delta Revenue | 2014 | 2019 | 2023 | CAGR 2014-2023 | CAGR 2019-2023 |

|---|---|---|---|---|---|

| Loyalty & Other | $8 billion | $10.1 billion | $14.5 billion | 6.8% | 9.4% |

| Premium | $9.6 billion | $15 billion | $19.1 billion | 7.9% | 6.2% |

| Main Cabin | $22.4 billion | $22 billion | $24.5 billion | 1% | 2.7% |

| Total | $40 billion | $47.1 billion | $58.1 billion | 4.2% | 5.4% |

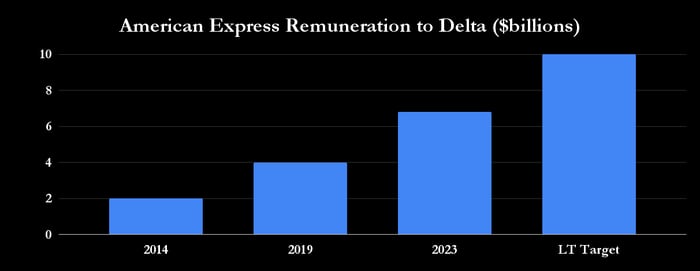

Third, Delta's highly successful SkyMiles program allows members to earn miles by traveling on Delta flights or spending on partner services, including co-branded credit cards with American Express. As management notes, partnership with American Express has led to spending through the Delta American Express credit cards to equate to almost 1% of U.S. GDP. As such, the relationship with American Express has turned into a significant income generator for Delta, as remuneration from American Express has grown significantly.

Management sees it hitting $10 billion over the long term.

The three points come together to create Delta's secret weapon. If wealth inequality increases, more spending will likely be concentrated in the higher percentile of income earners. That's good news for companies that have captured customers in those higher income brackets, and that's arguably what Delta's SkyMiles program has done.

On Investor Day last June, management said it had 25 million active members of the SkyMiles program, 30% of whom had a co-branded credit card.

Delta's senior vice president of Customer Engagement & Loyalty, Dwight James, noted, "Our portfolio is becoming more and more premium. The more premium my portfolio, the higher the average spend and the higher the remuneration from American Express." Moreover, Delta is driving SkyMiles' adoption among "younger, more engaged, and more premium" customers by offering free Wi-Fi and partnerships with companies like Starbucks.

That resulted in a lowering of the average age of new members from 44 in 2017 to 39 in 2022 and a shift in premium revenue from SkyMiles from 15% in 2017 to 29% in 2022.

In short, Delta is winning younger, more affluent SkyMiles members, resulting in a shift in revenue from the (fast-growing) program to the higher-margin premium services.

Aside from the headline risk of a slowdown in the economy and air travel, Delta could face risks from increased regulation in the credit card industry. In addition, customer dissatisfaction with loyalty programs may grow. After all, customers are spending money to build up miles, but the airline still decides what they can use those miles for. If customers don't see the benefit of raking up miles, the program and co-branded credit card usage could be under pressure.

Delta is not only enjoying the fruits of the aerospace recovery; it's also increasingly focusing its business on its premium customers and revenue generated from its loyalty programs. That makes it an attractive stock for investors, and it also looks like an excellent value when trading on slightly less than 7 times the estimated earnings for 2024.

Should you invest $1,000 in Delta Air Lines right now?

Before you buy stock in Delta Air Lines, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Delta Air Lines wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Starbucks. The Motley Fool recommends Delta Air Lines. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

© 2024 Lime Trading (CY) Ltd

Lime Trading (CY) Ltd is authorised and regulated by the Cyprus Securities and Exchange Commission in accordance with license No.281/15 issued on 25/09/2015. The "Just2Trade" trademark is owned by LimeTrading (CY) Ltd.

Registration Number: HE 341520

Address: Lime Trading (CY) Ltd

Magnum Business Center, Office 4B, Spyrou Kyprianou Avenue 78

Limassol 3076, Cyprus

Disclaimer:

All promotions, materials and information of this website may have applied conditions. Please contact the Company for further details

Trading on financial markets carries risks. The value of the investments can both increase and decrease and the investors may lose all their investment capital. In case of a leveraged product, the loss may be more than the initial capital invested. Detailed information on risks associated with trading on financial markets can be found in General Terms and Conditions for the Provision of Investment Services.

E-mail: 24_support@j2t.com