News

We provide the latest news from the world of economics and finance

We provide the latest news from the world of economics and finance

Zions Bancorporation ZION remains well-positioned for revenue growth on the back of strong loans and deposits, fee-income expansionary efforts, high rates and asset yield repricing. However, an elevated expense base and poor asset quality remain concerns.

Zions’ organic growth strategy is demonstrated through its revenue growth trajectory. The company’s total revenues witnessed a 2.3% compound annual growth rate (CAGR) over the last five years ended in 2023. The growth was primarily driven by robust loan growth, with loans and leases (net of unearned income and fees) experiencing a CAGR of 4.4% over the last four years ended in 2023.

ZION’s efforts to enhance fee income, decent loan demand and higher interest rates are likely to aid top-line expansion. Given the tough operating backdrop, we project total revenues (FTE) to fall 3.9% in 2024, while rebound and grow at the rate of 4.4% and 4.9% in 2025 and 2026, respectively. Further, we estimate total loans to witness a 2.3% CAGR by 2026.

Amid the high interest rate environment, Zions’ net interest margin (NIM) is expected to witness modest growth, while high funding costs will weigh on it to some degree. NIM increased to 3.06% in 2022 on account of a rise in interest rates. Though the metric declined in 2023 due to higher funding costs, we expect the same to be positively impacted in the near term driven by the current high rates and asset-yield repricing. We estimate NIM to be 3.02%, 3.22% and 3.37% in 2024, 2025 and 2026, respectively.

However, a persistent escalation in the expense base remains a challenge. While total non-interest expenses declined in 2020, the same witnessed a five-year CAGR of 4.5% for the year ended 2023. Given the ongoing investments in franchise and digital operations, the expense base is expected to remain elevated. Our estimates suggest adjusted non-interest expenses to witness a CAGR of 2.8% by 2026.

ZION’s deteriorating asset quality is another major headwind. Though the company recorded a provision benefit in 2021, a significant rise was recorded for the same in 2022 and 2023. The current tough macroeconomic outlook is anticipated to sustain the uptrend. While we estimate provision for credit losses to decline in 2024 and 2025, the metric will likely rise in 2026.

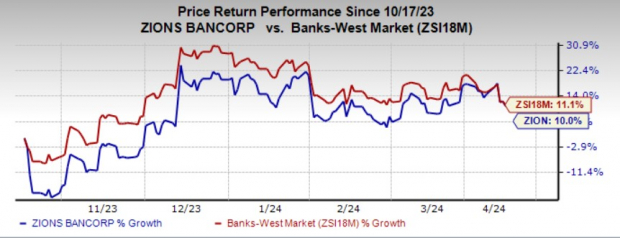

ZION currently carries a Zacks Rank #3 (Hold). Over the past six months, shares of the company have rallied 10%, underperforming the industry’s growth of 11.1%.

Image Source: Zacks Investment Research

Some better-ranked finance stocks worth mentioning are BlackRock Inc. BLK and Northern Trust Corporation NTRS.

BlackRock’s earnings estimates for the current year have been revised upward by 1.6% in the past seven days. The company’s shares have jumped 20% over the past six months. At present, BLK sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks Rank #1 stocks here.

Estimates for Northern Trust’s earnings for the current year have been revised upward by 1.9% in the past week. The company’s shares have gained 18.6% over the past six months. At present, NTRS also sports a Zacks Rank #1.

Infrastructure Stock Boom to Sweep America

A massive push to rebuild the crumbling U.S. infrastructure will soon be underway. It’s bipartisan, urgent, and inevitable. Trillions will be spent. Fortunes will be made.

The only question is “Will you get into the right stocks early when their growth potential is greatest?”

Zacks has released a Special Report to help you do just that, and today it’s free. Discover 5 special companies that look to gain the most from construction and repair to roads, bridges, and buildings, plus cargo hauling and energy transformation on an almost unimaginable scale.

Download FREE: How To Profit From Trillions On Spending For Infrastructure >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

© 2024 Lime Trading (CY) Ltd

Lime Trading (CY) Ltd is authorised and regulated by the Cyprus Securities and Exchange Commission in accordance with license No.281/15 issued on 25/09/2015. The "Just2Trade" trademark is owned by LimeTrading (CY) Ltd.

Registration Number: HE 341520

Address: Lime Trading (CY) Ltd

Magnum Business Center, Office 4B, Spyrou Kyprianou Avenue 78

Limassol 3076, Cyprus

Disclaimer:

All promotions, materials and information of this website may have applied conditions. Please contact the Company for further details

Trading on financial markets carries risks. The value of the investments can both increase and decrease and the investors may lose all their investment capital. In case of a leveraged product, the loss may be more than the initial capital invested. Detailed information on risks associated with trading on financial markets can be found in General Terms and Conditions for the Provision of Investment Services..

E-mail: 24_support@just2trade.online