What is a Bond? Complete European Investment Guide for 2026

Table of Contents

Bond Definition and Basic Mechanics

Types of Bonds: EU Market Classifications

How Bonds Work: Mechanics and Cash Flows

Bonds vs Stocks: Key Investment Differences

Why Invest in Bonds: Portfolio Benefits

Bond Risks: What Investors Should Know

How to Invest in Bonds: European Options and Strategies

Advanced Bond Concepts for EU Investors

Conclusion: Building Your Bond Investment Strategy

Frequently Asked Questions About Bonds

A bond is a fixed income security that represents a loan made by an investor to a borrower – typically a corporation or a government. In Europe, the most widely followed government bonds include German Bunds, French OATs, and Italian BTPs, while companies across the eurozone issue corporate bonds (Unternehmensanleihen). Bonds pay regular interest (called coupons) and return the principal amount at maturity, making them essential portfolio diversification tools for risk reduction and steady income generation.

Think of it this way: when you buy a bond, you're essentially becoming the bank. You're lending directly to a government or business – and they pay you for the privilege. With the global bond market valued at roughly $142 trillion at the end of 2024 (surpassing global equities at around $127 trillion), this asset class is the backbone of the financial system, even if stocks grab all the headlines. The European Union accounts for roughly 20% of global corporate and government bonds outstanding, making it the world's second-largest bond market after the United States.

Bond Definition and Basic Mechanics

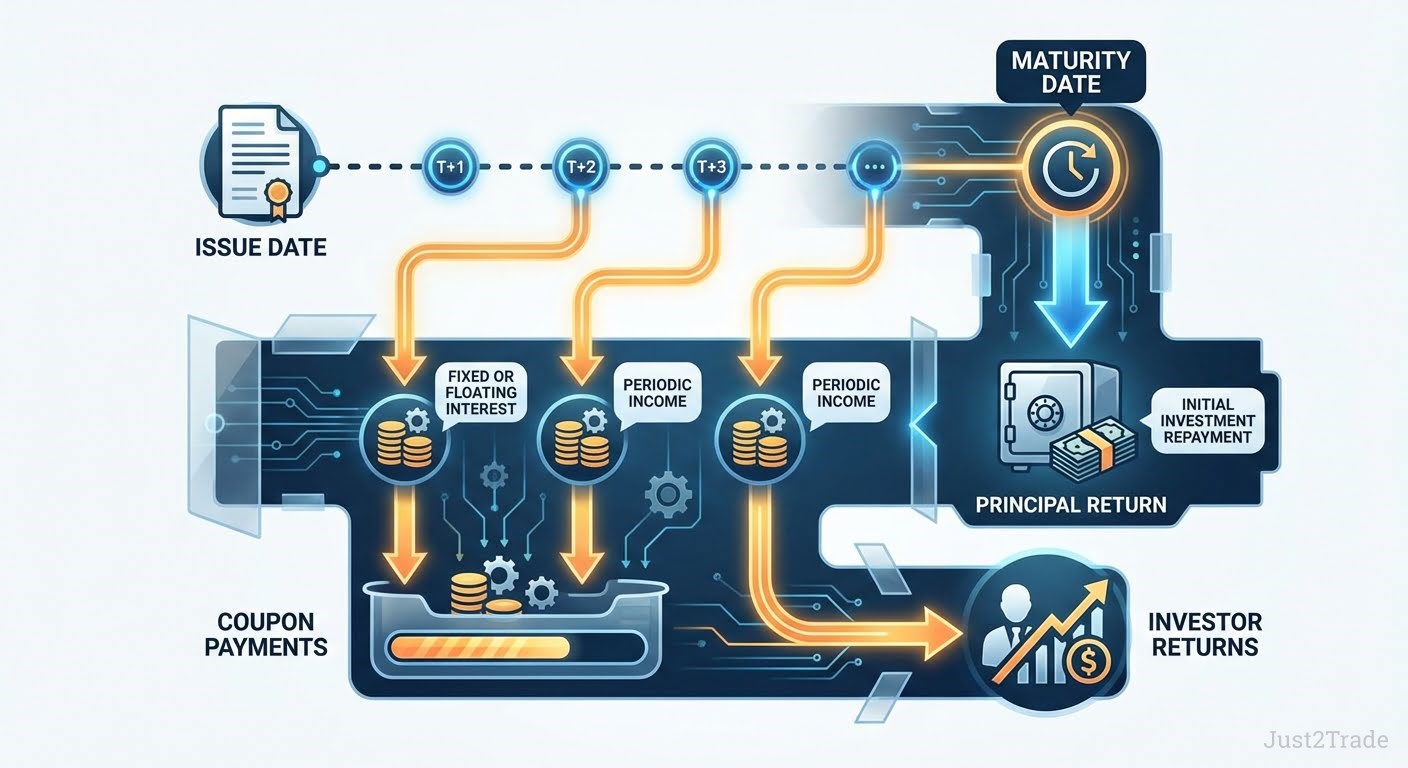

So what is a bond in its simplest form? A bond is a debt instrument – an IOU issued in the financial markets. When a government or corporation needs to raise capital, it can issue bonds rather than taking out a traditional bank loan. Investors who purchase these bonds are effectively lending money to the issuer in exchange for two things: regular interest payments and the return of their original investment at a specified future date.

In the European Union, bond markets are regulated under the framework of the European Securities and Markets Authority (ESMA) and national supervisors such as Germany's BaFin and France's AMF. Under the EU Prospectus Regulation, securities offered to the public generally require an approved prospectus. European investor compensation schemes vary by country – in Germany, for instance, the EdW covers 90% of claims up to €20,000 per investor in the event of broker insolvency.

European Regulatory Note: BaFin's 2026 Risks in Focus report highlights that while European banks and insurers are mostly profitable and well capitalised, geopolitical tensions, trade conflicts, and elevated sovereign debt levels remain key risks for financial stability. For bond investors, this underscores the importance of understanding credit risk and monitoring the macroeconomic environment closely.

Here's the basic bond meaning in practice. Suppose the German government issues a Bund with a face value of €1,000, a coupon rate of 2.5%, and a maturity of 10 years. As the bondholder, you receive €25 per year in interest. When the bond matures, you get your €1,000 back. Simple, predictable, and – crucially – contractually obligated.

Unlike stocks, where dividends are discretionary and share prices swing with market sentiment, bonds provide a legally binding commitment. The issuer must pay you. If they can't, that's a default – and bondholders rank ahead of shareholders in recovering assets.

The Essential Components of Every Bond

Every bond, whether a gilt or a corporate issue, shares four core components:

| Component |

Description |

Example (German Bund) |

| Face Value (Par) |

The principal amount repaid at maturity |

€100 per unit |

| Coupon Rate |

The annual interest rate paid to bondholders |

2.5% (€2.50/year) |

| Maturity Date |

The date when the issuer repays the face value |

15 August 2036 |

| Yield to Maturity |

Total expected return if held until maturity |

Varies with market price |

The Deutsche Finanzagentur (Germany's Federal Finance Agency) manages issuance of all federal securities. As of early 2026, approximately €1,311.5 billion in 7-, 10-, 15- and 30-year Federal bonds were outstanding – representing around 66% of the Federal government's total debt portfolio. An investor purchasing a Bund at a discount to par would earn both coupon income and a capital gain at redemption – illustrating how bonds generate returns through multiple channels.

Types of Bonds: EU Market Classifications

)

The European bond market offers several categories of fixed income securities, each with distinct risk levels, yields, and tax treatment. Understanding these bond categories – and how the bonds definition applies differently to each – helps investors match their risk tolerance with the appropriate debt instruments.

Government securities sit at one end of the spectrum, offering the lowest risk and correspondingly modest yields. Corporate bonds occupy the middle ground, while high-yield bonds offer elevated returns with greater credit risk. Europe also features a unique asset class – the Pfandbrief (covered bond) – which originated in Germany in the 18th century. Pfandbriefe are bank-issued bonds collateralised by mortgages or public sector loans under the Pfandbrief Act (Pfandbriefgesetz). No single Pfandbrief has ever defaulted in over 250 years of history, making them a cornerstone of conservative European portfolios.

Here's a practical comparison:

| Bond Type |

Issuer |

Risk Level |

Typical Yield (2026) |

Tax Treatment |

| German Bunds |

Federal Republic of Germany |

Very Low |

2.7%–3.4% |

Abgeltungssteuer (flat ~26.375%) |

| Corporate (IG) |

Blue-chip companies |

Low–Medium |

3.5%+ |

Abgeltungssteuer |

| High-Yield |

Lower-rated companies |

Medium–High |

5%–7%+ |

Abgeltungssteuer |

| Pfandbriefe |

German banks (covered bonds) |

Very Low |

Bund + small spread |

Abgeltungssteuer |

European Government Bonds

European government bonds are euro-denominated securities issued by eurozone sovereigns. German Bunds, issued through the Deutsche Finanzagentur, serve as the benchmark risk-free rate for the entire eurozone. French OATs (Obligations Assimilables du Trésor) and Italian BTPs (Buoni del Tesoro Poliennali) are the other two pillar markets, each with distinct risk-return profiles reflecting their sovereign credit quality.

As of late February 2026, the 10-year Bund yield sits around 2.70%, while the 30-year Bund yields approximately 3.40%. According to Bloomberg, the 30-year Bund yield briefly climbed to its highest level since 2011 in early February 2026, as investors demanded higher premiums to absorb a record debt burden linked to Germany's new infrastructure and defence spending commitments.

Germany has never defaulted on its sovereign debt obligations. This track record, combined with the country's AAA credit rating and constitutional "debt brake" (Schuldenbremse), gives Bunds their reputation as the eurozone's premier safe-haven asset. French OATs (rated AA-) and Italian BTPs (rated BBB) offer progressively higher yields, reflecting higher perceived sovereign risk.

Inflation-linked European government bonds adjust both coupon payments and principal value according to the eurozone Harmonised Index of Consumer Prices (HICP). With eurozone inflation at 1.7% in January 2026 – below the ECB's 2% target – and German HICP at 2.1%, these instruments offer a hedge for investors concerned about future inflation surprises.

Corporate Bonds: Company Debt Securities

When a company needs capital – say, for expansion, acquisitions, or refinancing – it can issue corporate bonds rather than diluting shareholders through equity issuance. This answers what is a bond in business: a financing tool that provides capital without surrendering ownership.

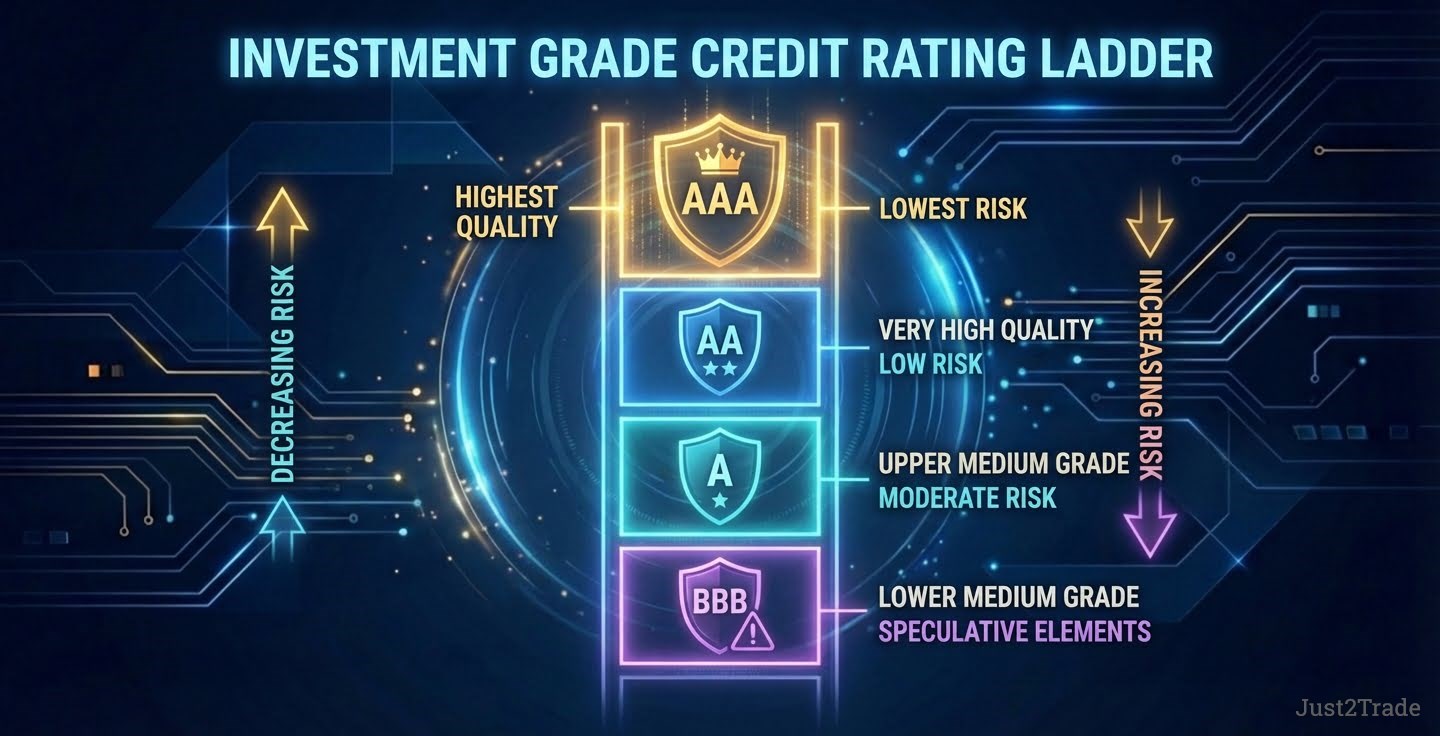

Corporate bonds typically offer a risk premium above gilts to compensate for the increased chance of default. Credit rating agencies such as Moody's, S&P, and Fitch assess each issuer's ability to repay, assigning ratings that influence pricing and investor demand.

Investment grade bonds (rated BBB or above by S&P) represent issuers with lower default probability. This classification matters enormously: EU pension funds and insurance companies are typically mandated to hold investment grade bonds, making these issues the institutional backbone of the fixed income market. Historically, BBB-rated corporate bonds have had a default rate approaching zero over most 12-month periods. Even BB-rated bonds – the highest tier of high-yield – have averaged just a 0.36% default rate over 23 years.

On the other hand, high-yield corporate bonds carry ratings below BBB, and their higher coupons reflect genuine credit risk. During stress periods like the 2008–09 financial crisis, sub-investment-grade default rates across Europe reached approximately 10%.

European high-yield bond volumes surged 85.9% in 2024 compared to the previous year, as borrowers front-loaded refinancing ahead of anticipated maturity walls. For European investors, the current environment offers compelling opportunities across the credit spectrum – provided you understand the risk-return trade-offs.

| Rating |

Category |

Risk Level |

Default Probability |

| AAA / AA |

Investment Grade |

Minimal |

Extremely Low |

| A |

Investment Grade |

Low |

Low |

| BBB |

Investment Grade |

Moderate |

Relatively Low |

| BB |

High-Yield |

Elevated |

Notable |

| B and below |

High-Yield |

High |

Significant |

How Bonds Work: Mechanics and Cash Flows

)

Understanding how bonds work requires grasping three interconnected concepts: coupon payments, pricing dynamics, and yield calculations. While the bonds definition centres on the lending relationship, the mechanics determine what you actually earn.

- Coupon payments are the periodic interest payments an issuer makes to bondholders. The coupon payment frequency on bonds determines how the periodic interest pay-outs are made to investors. When an individual purchases a bond, the coupon rate mentioned indicates the annual rate of interest that will be paid on the bond.

- The price-yield relationship is the heartbeat of bond markets, and it's inversely proportional: when yields rise, bond prices fall, and vice versa. Why? If new bonds are issued at 5% while your existing bond pays 4%, no rational investor would pay full price for your lower-paying bond. Its price must drop until the effective yield matches current market rates.

Here's a practical calculation. Suppose a German Bund was issued at €100 with a 2.5% coupon. If the market yield rises to 3.5%, the price drops to approximately €92 (depending on remaining maturity). At this price, the €2.50 annual coupon represents a current yield of about 2.7% (€2.50 ÷ €92), plus the buyer earns a capital gain at redemption – and the combined yield to maturity aligns with the prevailing market rate.

- Duration measures a bond's sensitivity to interest rate changes. A bond with a duration of 7 means that for every 1% rise in interest rates, the bond's price falls by roughly 7%. Long-dated Bunds (say, 30 years) have much higher duration than short-dated ones (2–3 years). The Deutsche Finanzagentur notes that price risk is "significantly higher for 30-year Bunds (high) than for 10-year Bunds (medium)" – though holding to maturity eliminates this risk entirely.

Understanding Bond Pricing and Yields

Bond pricing in the secondary market depends on supply and demand, prevailing interest rates, and the issuer's creditworthiness. When a bond trades above its face value (say, £105 for a £100 par bond), it's trading at a premium. Below face value – that's a discount.

There are several yield measures to understand:

- Current yield: Annual coupon divided by the current market price

- Yield to maturity (YTM): The total annualised return if held to maturity, factoring in both coupons and any capital gain or loss

- Running yield: Similar to current yield, representing the income return based on today's price

When comparing bonds, always use yield to maturity – it's the most comprehensive measure. Real-time pricing for European government bonds is available through the Deutsche Finanzagentur, the ECB Statistical Data Warehouse, and major European exchanges.

Bonds vs Stocks: Key Investment Differences

If you're wondering how bond stock differences play out in practice, think of it as the distinction between being a lender and being an owner. When you buy shares, you acquire partial ownership of a company and participate in its profits (or losses). When you buy a bond, you're a creditor – you've lent money, and you want it back with interest.

| Feature |

Bonds |

Stocks |

| Relationship |

Creditor (lender) |

Owner (shareholder) |

| Income |

Fixed coupon payments |

Variable dividends |

| Capital Return |

Face value at maturity |

No guaranteed return |

| Priority in Liquidation |

Senior to shareholders |

Last in queue |

| Risk Level |

Generally lower |

Generally higher |

| Growth Potential |

Limited to yield |

Unlimited upside |

This creditor-versus-owner dynamic is what makes bonds an alternative to equity investment in portfolio construction. Stocks offer higher potential returns – roughly 10% annually on average – while long-term government bonds have historically earned around 5%. But that gap comes with significantly more volatility.

Risk-Return Trade-offs in Investment Selection

The correlation benefits of holding both asset classes are where things get interesting for portfolio construction. During periods of market stress, government bond prices in major economies like the EU often rise as investors seek safety – the so-called flight to quality. This negative correlation with equities means bonds can smooth out your portfolio's long-term performance.

Historically, European equities (Euro Stoxx 50) have exhibited annualised volatility of around 15–18%, while Bund returns have shown standard deviation closer to 5–7% – roughly half the price swings for a meaningful portion of the return. A classic balanced portfolio might allocate 60% to equities and 40% to bonds, though asset allocation varies based on age, risk tolerance, and investment horizon.

The key insight? Bonds and stocks aren't competitors – they're complementary components of a diversified portfolio.

Why Invest in Bonds: Portfolio Benefits

Bonds serve three essential roles in a well-constructed portfolio: income generation, risk reduction, and capital preservation. Let's examine each.

- Steady income generation is perhaps the most straightforward benefit. Unlike stock dividends, which companies can cut or suspend at will, bond coupon payments are contractual obligations. For income-focused investors – particularly those in or approaching retirement – this predictability is invaluable. With German Bunds yielding between 2.7% and 3.4% depending on maturity, peripheral eurozone sovereigns offering higher yields, and investment grade corporate bonds providing 3.5%+, the current yield environment offers meaningful income across the European fixed income spectrum.

- Portfolio diversification through bonds reduces overall volatility. When equity markets tumble – as they did during the tariff-driven sell-off in April 2025 – high-quality government bonds tend to hold their value or even appreciate. Bonds help smooth out a portfolio's long-term performance by behaving differently from shares – a principle well documented in ECB research on euro area financial stability.

- Capital preservation matters most for investors with shorter time horizons or lower risk tolerance. If you hold a Bund to maturity, you know exactly what you'll receive – every coupon payment and the full face value at redemption (assuming no government default, which has never happened in German sovereign debt history).

)

There's also a tactical dimension: rebalancing opportunities. When equity prices fall, bonds typically hold steady or rise, creating a natural mechanism to "buy low" on stocks by selling appreciated bonds. As a general principle, higher-quality bonds offer lower interest rates but provide the stability that volatile equity portfolios need – a trade-off that sits at the heart of modern portfolio theory.

Bonds in Retirement and Pension Planning

Bonds play a particularly crucial role in retirement planning. Long-duration bonds back annuity products – the guaranteed income streams that pension holders can purchase with their retirement pots. When you buy an annuity, the insurance company invests predominantly in bonds to fund your lifetime payments. Annuity-targeting funds typically invest in bonds whose prices move broadly in line with annuity costs, reflecting how interest rate changes affect annuity pricing as you approach retirement.

For European investors, tax treatment varies by jurisdiction. In Germany, bond income (coupons and capital gains) is subject to the Abgeltungssteuer – a flat withholding tax of 25% plus 5.5% solidarity surcharge (totalling approximately 26.375%), with a tax-free allowance (Sparer-Pauschbetrag) of €1,000 per individual or €2,000 for couples. In France, the prélèvement forfaitaire unique (PFU) applies a flat 30% rate. Each EU country has its own rules, so consult a local tax adviser for your specific situation.

A common guideline suggests your bond allocation should roughly equal your age – so a 40-year-old might hold 40% in bonds and 60% in equities. It's a starting point, not a rule. Your actual allocation depends on personal circumstances, risk appetite, and income needs.

Bond Risks: What Investors Should Know

The bonds definition often implies safety, but that's an oversimplification. Every bond carries risks that investors must understand before committing capital.

- Credit risk (default risk) is the possibility that the issuer cannot meet its payment obligations. For EU gilts, this risk is negligible – the government has always honoured its debts. For corporate bonds, credit risk varies dramatically based on the issuer's financial health. Credit rating agencies (Moody's, S&P, Fitch) assign ratings that influence pricing and investor demand.

- Investment grade bonds (BBB and above) have historically experienced default rates approaching zero, while EU speculative-grade default rates can spike to 3–4% during economic downturns.

- Interest rate risk is arguably the most misunderstood bond risk. When the European Central Bank raises or maintains its key rates (the deposit facility rate currently stands at 2.00%, with the main refinancing rate at 2.15% as of February 2026), new bonds are issued with coupon rates reflecting current conditions. Existing bonds with lower coupons become less attractive, and their market prices fall. The longer the bond's maturity, the more sensitive it is to rate changes.

- Inflation risk erodes the real value of fixed coupon payments. If your bond pays 2.5% but inflation runs at 2.1% (as in January 2026 for Germany), your real return is a slim 0.4%. Inflation-linked European government bonds address this by adjusting payments to the eurozone HICP, but conventional bonds offer no such protection.

- Liquidity risk refers to the difficulty of selling a bond quickly at a fair price. German Bunds are among the most liquid government bonds globally – the Deutsche Finanzagentur reports that 10-year Bunds alone accounted for €2,474 billion in trading volume in 2024, representing 37% of all Federal securities turnover. The Finanzagentur and the Deutsche Bundesbank also maintain the market and, if necessary, act as trading partners. Some corporate bonds – particularly those from smaller issuers – may have thin secondary markets.

Managing Bond Investment Risks

Effective risk management involves several practical strategies:

- Duration laddering spreads your bond investments across multiple maturity dates, reducing the impact of any single interest rate move. Rather than investing everything in a 10-year gilt, you might buy a mix of 2-, 5-, 10-, and 20-year issues.

- Credit diversification means spreading exposure across different issuers and sectors. A bond fund that holds hundreds of different corporate issues provides far better protection against individual defaults than a concentrated portfolio.

- Professional management through bond funds or ETFs offers expertise in credit analysis, duration positioning, and market timing that most individual investors lack. Fund managers can actively adjust portfolios in response to changing conditions – a significant advantage in volatile rate environments.

How to Invest in Bonds: European Options and Strategies

European investors have multiple pathways to access the bond market, each with distinct advantages depending on portfolio size and expertise.

- Direct government bond purchases are available through the Deutsche Finanzagentur's retail service for German Bunds, or through any regulated broker in your jurisdiction. French OATs and Italian BTPs can likewise be purchased through brokers with access to Euronext Paris or MTS (Italy's electronic bond market).

- Bond funds and ETFs are the most popular investment vehicles for beginners. They provide instant diversification across hundreds of individual bonds, professional management, and lower minimum investments – some allow you to start with a few hundred euros. Euro government bond-tracking ETFs with total expense ratios as low as 0.07% offer extremely cost-efficient access to sovereign debt.

- Corporate bond funds offer exposure to investment grade company debt, typically yielding more than government bond funds but with slightly higher risk.

- Tax efficiency varies across Europe. In Germany, the Sparer-Pauschbetrag (€1,000 per individual) exempts a portion of investment income from the ~26.375% Abgeltungssteuer. In France, a PEA (Plan d'Épargne en Actions) shelters certain qualifying bonds from taxation after five years. In the Netherlands, investment income is taxed under Box 3 based on deemed returns rather than actual gains. Always consult a local tax adviser for jurisdiction-specific guidance.

Choosing Between Bond Funds and Direct Investment

The choice between bond funds and direct bond ownership depends on your circumstances:

- Bond funds suit investors who want diversification without large capital, prefer professional management, and don't need income on specific dates. They charge annual fees (typically 0.1%–0.5% for passive funds) but offer liquidity and convenience.

- Direct bonds suit investors with larger portfolios who want to lock in a specific yield to maturity and receive exact coupon payments on known dates. You'll know precisely what you earn if held to maturity – no fund manager can alter that outcome. However, direct corporate bonds often require minimum purchases of €1,000 per bond, and building a diversified portfolio requires significant capital.

For most beginners, bond funds or ETFs represent the smarter starting point. As your portfolio grows and your knowledge deepens, you can consider adding individual gilts or corporate issues for specific maturity targeting.

Advanced Bond Concepts for EU Investors

Once you've grasped the fundamentals, a few advanced concepts can sharpen your bond investment strategy.

- Duration is the key measure of interest rate sensitivity. Modified duration tells you how much a bond's price will change for a 1% shift in interest rates. A Bund with a duration of 15 would lose roughly 15% of its value if yields rose by one percentage point – a dynamic vividly illustrated when European long-dated bond yields spiked during the rapid ECB rate-hiking cycle in 2022–2023, from near-zero to above 4%. Short-duration bonds (under 5 years) offer much greater price stability.

- The yield curve plots bond yields across different maturities, and its shape provides powerful economic signals. A normal upward-sloping curve suggests economic optimism, while an inverted curve (short-term yields exceeding long-term ones) has historically preceded recessions. The ECB held its deposit facility rate steady at 2.00% in February 2026, with swap markets pricing in broadly stable rates for the remainder of 2026. Some economists, including Deutsche Bank, see the next move as a potential hike in mid-2027 if fiscal easing and tight labour markets push inflation above target.

- Convexity refines the duration calculation – measuring how duration itself changes as yields move. Bonds with positive convexity gain more from falling yields than they lose from rising ones.

- Bond ladder strategies involve purchasing bonds with staggered maturity dates (e.g., 1, 3, 5, 7, and 10 years). As each bond matures, you reinvest at current rates, smoothing out interest rate risk over time. A barbell strategy takes a different approach, concentrating holdings at short and long maturities while skipping intermediate terms – capturing higher long-end yields while maintaining liquidity through short-dated positions.

Conclusion: Building Your Bond Investment Strategy

Bonds deserve a place in virtually every investor's portfolio. They provide fixed income through regular coupon payments, capital preservation through senior creditor status, and diversification benefits through their low correlation with equities.

For investors exploring European government bonds, German Bund yields near 2.7%–3.4% in 2026 provide the risk-free foundation, peripheral eurozone sovereigns offer higher yields for those comfortable with additional sovereign risk, and the ECB's steady rate stance provides a stable environment for fixed income investors.

Here's a practical roadmap for getting started:

- Assess your allocation: Use your age as a starting guideline for bond percentage

- Start with government bond funds or ETFs: Low cost, diversified, and straightforward

- Optimise for tax: Use your country's tax-advantaged wrappers – Germany's Freistellungsauftrag, France's PEA, or equivalent structures – wherever possible

- Diversify gradually: Add corporate bonds as your comfort grows

- Monitor duration: Match your bond duration to your investment horizon

Whether you're a cautious retiree or a younger investor building a balanced portfolio, understanding the full bond meaning gives you a powerful tool for navigating any market condition. Practice on a demo account if you're new to fixed income, and consult a qualified financial adviser (Finanzberater) for complex situations.

This article is for informational purposes only. It should not be considered financial, legal, or investment advice. Bond prices can fall as well as rise. Always consult a certified professional before making financial decisions.

FAQ

-

What's the difference between bonds and savings accounts?

Bonds typically offer higher returns than savings accounts but carry market risk – your capital value can fluctuate before maturity. In the EU, deposit guarantee schemes protect savings up to €100,000 per depositor per bank under the Deposit Guarantee Schemes Directive. European savings accounts currently offer modest returns, while Bunds and corporate bonds may offer more – with correspondingly more risk.

-

How much of my portfolio should be in bonds?

A common rule of thumb is to match your bond allocation to your age: a 30-year-old might hold 30% bonds, while a 60-year-old might hold 60%. However, your specific risk tolerance, income needs, and investment timeline all matter. Conservative investors may prefer higher allocations regardless of age.

-

Are bond funds better than individual bonds for beginners?

Generally, yes. Bond funds offer instant diversification, professional management, and lower minimum investments. You can start with a few hundred pounds rather than the £1,000+ required for many direct corporate bond purchases. Individual bonds suit larger, more experienced investors who want maturity control.

-

What happens to bonds during economic recessions?

Government bonds tend to perform well during recessions as investors pursue safety – a phenomenon known as flight to quality. When stock markets fall, money flows into Bunds and treasuries, pushing their prices up. Corporate bonds, especially high-yield issues, may suffer as default concerns rise.

-

How do I research bond credit ratings before investing?

Start with the major rating agencies: Moody's, S&P Global, and Fitch. Their publicly available ratings classify issuers from AAA (safest) to C/D (default). For deeper analysis, review the issuer's financial statements – focusing on debt-to-equity ratios, interest coverage, and cash flow trends. Most EU investment platforms display credit ratings alongside bond listings.

-

Can I lose money investing in EU government bonds?

Yes – if you sell before maturity at a lower price than you paid. Interest rate rises cause existing bond prices to fall, and during the ECB's 2022--2023 rate-hiking cycle, long-term European bond prices fell sharply. However, if you hold a Bundto maturity, you'll receive the full face value back (assuming no government default).

-

What's the tax treatment of bond income in the EU?

Tax treatment varies across Europe. In Germany, both coupon income and capital gains on bonds are subject to the Abgeltungssteuer (~26.375%), with a €1,000 annual tax-free allowance (€2,000 for couples). In France, the flat 30% PFU applies. In Italy, government bond income is taxed at a preferential 12.5%, while corporate bonds face 26%. Each EU country has its own rules – consult a local tax adviser for your specific jurisdiction.

-

How often do bonds default in the EU market?

German government Bunds have never defaulted. For investment grade corporate bonds (BBB and above), historical default rates are near zero in most years. Even BB-rated bonds average just 0.36% annually over two decades. Default risk rises significantly for lower-rated issuers, particularly during recessions when European speculative-grade defaults can reach 3–4%.

)